Two Strategies, Diverging in 2026

ACROSS THE UNITED STATES — the strategic question facing ABA operators in 2026 is not whether to grow but how to deliver. The dominant move at the largest providers is to integrate. Cortica, Hopebridge, Westside Children’s Therapy, the Stepping Stones Group, Autism Learning Partners, and Soar Autism Center all run, or are building, models that combine ABA with speech-language pathology, occupational therapy, and in many cases physical therapy, psychology, and feeding programs. ABA Matrix listed the multidisciplinary pivot as one of six defining trends for the field in 2026.

The counter-position belongs to ACES, officially known as Comprehensive Educational Services, owned by General Atlantic since 2020. On December 19, 2026, ACES announced its acquisition of Phoenix-based Ally Pediatric Therapy from SBJ Capital, which had backed Ally since 2022. The deal moved Ally’s nine locations into the ACES footprint, bringing the platform to 92 sites across seven states. ACES also announced that it would wind down Ally’s in-house speech, occupational therapy, and feeding programs and replace them with external care coordination through community providers in the Phoenix area.

The move makes ACES’ position visible. Where most national operators are buying additional service lines, ACES is unbundling them. Both strategies are responses to the same pressures: payers asking for outcomes, families asking for coordination, and PE owners asking which model produces a more defensible exit multiple. The two camps are arriving at opposite answers.

“I think it’s clinically necessary. When we look at the outcomes that we see in the data, when you combine ABA with other specialties, the outcomes for the children are better.” – Dan Hartman, partner, Morgan Health, at INVEST 2025.

What the Integrators Are Building

The case for multidisciplinary integration runs on three legs: clinical outcomes, payer preference, and operational economics. Cortica is the most cited example. CEO Neil Hattangadi told the INVEST 2025 conference that providers willing to deliver care through adolescence and into adulthood, integrating ABA with the related disciplines that autistic clients tend to need over time, would define the next phase of the industry.

Hopebridge runs what the company calls its 360 Care model, which combines ABA with occupational therapy, speech therapy, and feeding therapy under a single roof. Westside Children’s Therapy CEO Mark Cassidy framed the shift in Behavioral Health Business’s 2026 outlook survey as a move away from legacy 40-hour-per-week ABA-only models toward holistic, multidisciplinary approaches delivered at clinically appropriate, cost-effective dosages.

The economic logic for integrators is twofold. Multidisciplinary platforms can capture more of the family’s care wallet under a single authorization umbrella, and they can demonstrate cross-disciplinary outcomes that single-discipline providers cannot. PE valuations reflect both. FOCUS Investment Banking’s April 2026 benchmarks put platform ABA at 8 to 12 times EBITDA, with pediatric therapy adjacencies adding optionality on payer negotiation and outcomes reporting.

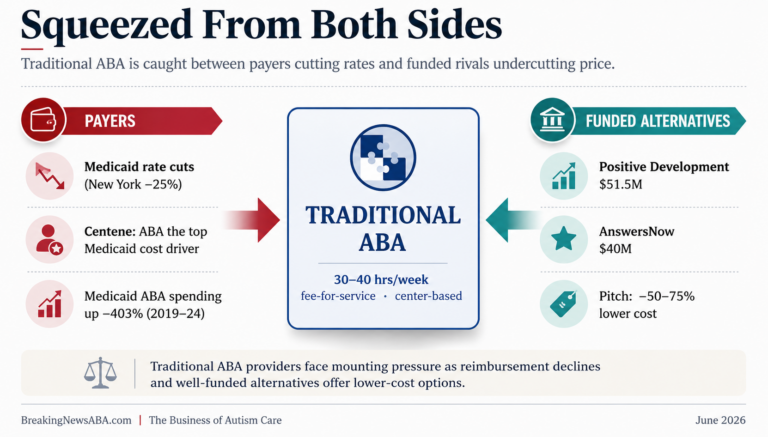

The 40-hour week is also being recalibrated. CASP’s May 2024 Version 3.0 Practice Guidelines describe comprehensive treatment at 30 to 40 hours per week and focused treatment at lower hour levels. Multidisciplinary operators argue that a clinically appropriate 25-hour ABA week paired with weekly speech and OT often produces better functional outcomes than a 40-hour ABA-only schedule, at a lower combined cost. State Medicaid programs, particularly Indiana (tiered weekly limits of 30, 32, or 38 hours plus a 4,000-hour lifetime cap, effective April 1, 2026) and North Carolina (16-hour weekly cap under HB 696, April 30, 2026), are pricing that view into policy.

What ACES Is Betting On

The ACES position is the cleanest counterargument in the market. ACES already operated an ABA-only model across its previous 83 locations in California, Colorado, Hawaii, North Carolina, Oklahoma, Texas, and Arizona. The Ally transaction extended the model, not bridged to a new one. Ally’s in-house multidisciplinary services are being decommissioned, not absorbed.

The ACES announcement framed the move in clinical terms: bringing the acquired assets into line with ACES’ ABA-centric care model. The operational case is also straightforward. ABA-only platforms reduce credentialing complexity (one license type per clinician), simplify billing (CPT 97151, 97153, 97155 dominate the code mix), and tighten staffing economics (a single staffing pyramid of BCBAs supervising RBTs, rather than parallel pyramids for OT, speech, and PT).

General Atlantic acquired ACES in 2020. ACES CEO Lisa Dawe said in the January release that the platform plans to add more Arizona clinics and invest in tools and training for clinicians. The strategic implication is that General Atlantic, after six years of holding the platform, has concluded that focused ABA with external care coordination is the preferred path to scale, at least for ACES.

Where most national operators are buying additional service lines, ACES is unbundling them. Both moves are responses to the same payer and outcomes pressures, arrived at from opposite directions.

Payer Pressure Is Behind Both Strategies

Payers are pushing in two directions at once. Commercial insurers and state Medicaid programs increasingly want outcome data, not service hours. Both integrated and focused operators argue their model produces better outcomes data. Integrated providers point to cross-disciplinary functional gains. Focused providers point to clinical purity, easier audit defense, and cleaner attribution of progress to the ABA protocols themselves.

Documentation and audit risk are now industry-defining variables. The HHS Office of Inspector General has completed four state-level ABA audits since 2024, with cumulative improper or potentially improper payment findings exceeding $575 million across Indiana, Wisconsin, Maine, and Colorado, including $285 million in Colorado alone, according to VG Soft Co’s State of ABA Therapy 2026 industry report. Provider organizations now spend meaningful operational time defending the relationship between authorized hours, documented sessions, and billed claims. The two strategies sketched out above each carry different audit profiles.

Jim Spink, CEO of Autism Care Partners, told the Autism Investor Summit East that until the field defines standardized data sets, there will be few real value-based contracts. Outcomes data is the structural bridge between either delivery model and the value-based reimbursement framework payers are signaling.

What Strategic and PE Buyers Are Paying For

Hexagon Capital Alliance, in its June 2025 ABA M&A commentary, described a re-energizing middle-market PE pipeline focused on best-in-class ABA businesses. The transactions Hexagon advised on in early 2025 included Alongside ABA (formed from Autism Spectrum Interventions, which was acquired by Fletch Equity in March 2024, then acquiring Quality Behavior Solutions and San Diego ABA in 2025); Behavior Frontiers (sold to NexPhase Capital in May 2025, twelve-state ABA-only footprint); and Unison Therapy Services (sold to Ascend Capital Partners with the Autism Impact Fund alongside, multidisciplinary ABA + speech + OT model).

The transaction record cuts both ways. Buyers paid for both ABA-only platforms (Behavior Frontiers) and multidisciplinary platforms (Unison) in the same quarter. The buyer pool is not yet uniformly rewarding either strategy. What the larger pattern shows is that buyers are paying for operational maturity, documentation rigor, payer relationship quality, and demonstrable margin, regardless of service-line breadth.

The aging-PE-platform pipeline reinforces both bets. 35 ABA and pediatric therapy platforms have been held by PE for five years or longer, according to Mergium Advisors’ year-end 2025 inventory. As those platforms come to market, the next round of buyers will price multidisciplinary breadth and ABA-only focus differently depending on the geographic and payer mix of each target.

The Decision for Clinic Owners

For an independent ABA clinic operator in 2026, the strategic question is not whether to add services but whether the local payer and clinical environment rewards integration or focus. In commercially-insured suburban markets with high family demand for one-stop care, the integrators have the advantage. In Medicaid-heavy markets with strict utilization controls, audit-active state policies, and a deep referral network of independent OTs and speech-language pathologists, the ACES model can compete.

Three practical tests cover most decisions. First, what do the dominant payers in your market reimburse for, and at what rate, for OT, speech, and feeding services? Second, is the local clinical workforce deep enough to credential and retain those clinicians, or is hiring already at the breaking point for BCBAs alone? Third, what is the documentation infrastructure required to defend either model under audit conditions like those Indiana, Maine, Wisconsin, and Colorado now face?

The 2027 CPT code overhaul, approved by the AMA in September 2025 and effective January 1, 2027, will retire current T-codes (0362T, 0373T) and add six new codes. The transition is the next forcing event for both models. Multidisciplinary providers must map cross-discipline workflows to the new code structure. ABA-only providers must align their external care-coordination relationships with the new documentation requirements.

The Q2 2026 round of behavioral-health M&A reports from Mertz Taggart and Mergium Advisors will indicate whether the strategic split between integrators and focused operators is widening or narrowing into the second half of the year. Both reports are scheduled for release by mid-summer.

AT A GLANCE

| Dominant trend among large operators: |

Multidisciplinary integration (ABA + OT + speech + feeding) |

| Named integrators: |

Cortica, Hopebridge, Westside, Stepping Stones, Soar Autism Center |

| Counter-example: |

ACES (General Atlantic-owned) stripping multidisciplinary services from Ally Pediatric Therapy |

| ACES + Ally deal date: |

January 16, 2026 |

| ACES footprint after Ally: |

92 locations across 7 states (was 83 across 7) |

| Hopebridge model: |

360 Care: ABA + OT + speech + feeding under one roof |

| Multidisciplinary advocate quote: |

Dan Hartman, Morgan Health partner, at INVEST 2025 |

| ABA-only platform quote: |

Lisa Dawe, ACES CEO, January 2026 release |

| CASP comprehensive treatment range: |

30 to 40 hours/week (Version 3.0, May 2024) |

| OIG ABA audit findings to date: |

$575M+ in improper/potentially improper payments across Indiana, Wisconsin, Maine, Colorado |

| 2027 CPT code overhaul: |

Effective January 1, 2027; retires 0362T and 0373T; adds 6 new codes |

| Next M&A read: |

Mertz Taggart and Mergium Q2 2026 reports, due mid-summer |

SOURCES & REFERENCES

| 1. |

ABA Matrix. ABA Trends 2026: A Look at the Forces Set to Shape the Behavior Analysis Field. December 10, 2025. https://www.abamatrix.com/aba-trends-2026/ |

| 2. |

Behavioral Health Business. Behavioral Health in 2026 Will Transition From Growth to Proof. December 31, 2025. https://bhbusiness.com/2025/12/31/behavioral-health-in-2026-will-transition-from-growth-to-proof/ |

| 3. |

Behavioral Health Business. ACES Acquires Ally Pediatric Therapy, Transitions to ABA-Only Model. January 16, 2026. https://bhbusiness.com/2026/01/16/aces-acquires-ally-pediatric-therapy-transitions-to-aba-only-model/ |

| 4. |

Behavioral Health Business. The Ascent of Multidisciplinary Autism Therapy Likely Defines Industry Future. December 2, 2025. https://bhbusiness.com/2025/12/02/it-feels-pretty-inevitable-the-ascent-of-multidisciplinary-autism-therapy-likely-defines-industrys-future/ |

| 5. |

Behavioral Health Business. Autism Care Faces Market Reckoning as Payers, Investors Push for Proof of Outcomes. November 21, 2025. https://bhbusiness.com/2025/11/21/autism-care-faces-market-reckoning-as-payers-investors-push-for-proof-of-outcomes/ |

| 6. |

VG Soft Co (Dustin Schwartz). State of ABA Therapy 2026: Industry Report for Practice Owners. April 14, 2026; updated May 12, 2026. https://vgsoft.co/blog/state-of-aba-therapy |

| 7. |

Hexagon Capital Alliance. Autism Treatment M&A Heating Up Again. June 2025. https://www.hexagoncapitalalliance.com/wp-content/uploads/2025/06/Hexagon-Capital-Alliance-Autism-June-2025.pdf |

| 8. |

FOCUS Investment Banking (Eric Yetter). Behavioral Health Valuation Benchmarks 2026. April 11, 2026. https://focusbankers.com/behavioral-health-practice-valuation/ |

| 9. |

Council of Autism Service Providers (CASP). Applied Behavior Analysis Practice Guidelines for the Treatment of Autism Spectrum Disorder, Version 3.0. Released May 7, 2024. https://www.casproviders.org/asd-guidelines |

| 10. |

General Atlantic. ACES and General Atlantic Announce Strategic Partnership. 2020. https://www.generalatlantic.com/media-article/aces-and-general-atlantic-announce-strategic-partnership/ |

| 11. |

ABA Coding Coalition. 2027 CPT Code Update for ABA Services. September 2025. https://abacodes.org/aba-cpt-codes-update/ |