A Multi-Specialty Pediatric Therapy Provider Attracts PE Capital

CONWAY, ARKANSAS — in January 2025, Leavitt Equity Partners announced its partnership with Pediatrics Plus, a specialized pediatric therapy provider headquartered in Conway, Arkansas, that serves more than 6,000 children with special needs and developmental delays each year. The transaction involved Leavitt Equity Partners as lead investor, with Fulcrum Equity Partners — an Atlanta-based growth equity firm specializing in healthcare services — and Western Governors University, through its investment arm Juvo Ventures, joining as additional partners. Terms were not disclosed.

Pediatrics Plus was founded in 2002 by Todd and Amy Denton and has grown into one of the more distinctive pediatric therapy providers in the South-Central United States. The company offers physical therapy, occupational therapy, speech and language pathology, and applied behavior analysis across its Arkansas and Texas operations. It also operates several related brands, including The Farm by Pediatrics Plus, Community Connections, and Rise Counseling and Diagnostics.

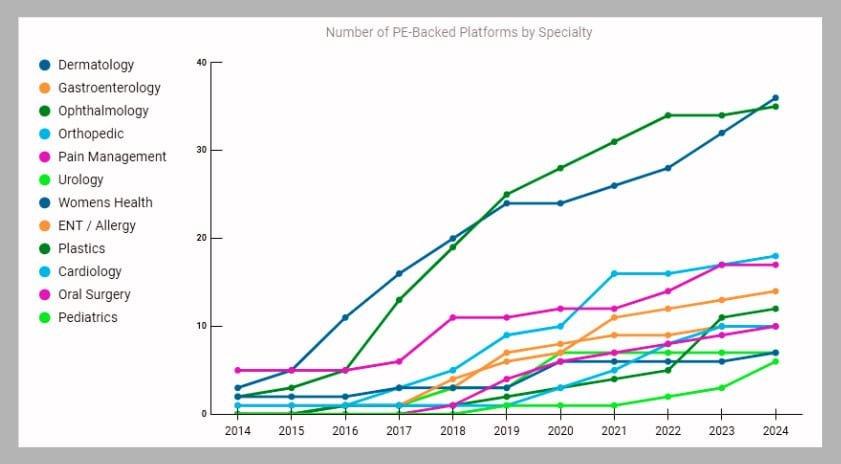

What makes Pediatrics Plus strategically significant for the ABA industry is its multi-specialty model. Most PE-backed ABA platforms are single-specialty providers — they offer ABA therapy exclusively or as their dominant service line. Pediatrics Plus integrates ABA with occupational therapy, speech therapy, and physical therapy in what the company describes as a blended service model designed to deliver the best outcomes for children. This integration creates both clinical and business advantages that pure-play ABA providers do not have.

The Pediatrics Plus transaction signals a shift in PE acquisition strategy in the autism services sector: from single-specialty ABA platforms to multi-specialty pediatric therapy providers that offer ABA alongside occupational, speech, and physical therapy under one roof.

Scott Street, CEO of Pediatrics Plus, stated that the partnership positions the company to expand into new markets and enhance its service offerings. The Denton family, who founded the company, remain the largest shareholders and continue to serve on the board of directors — a structural arrangement that preserves founder influence while providing the growth capital needed for geographic expansion.

Leavitt Equity Partners: A Healthcare PE Firm With a Government Pedigree

Leavitt Equity Partners is a Salt Lake City-based healthcare-focused private equity firm founded in 2014 by Michael O. Leavitt, who served as the 20th United States Secretary of Health and Human Services under President George W. Bush from 2005 to 2009 and as Governor of Utah from 1993 to 2003. The firm manages over $400 million in capital, raised primarily from strategic healthcare partners including provider systems, national and regional health insurers, healthcare service providers, healthcare IT companies, pharmaceutical companies, and healthcare executives.

The firm’s investor base is notable because it is drawn almost entirely from the healthcare industry itself. Unlike generalist PE firms that raise capital from pension funds, endowments, and family offices, Leavitt Equity Partners has assembled a limited partner base of healthcare operators and insurers. This creates a network of strategic relationships that can provide portfolio companies with operational partnerships, payer introductions, and industry expertise that financial-only investors cannot replicate.

The healthcare policy angle: Leavitt’s personal background as the former head of HHS gives the firm an institutional understanding of healthcare regulation, reimbursement policy, and government payer dynamics that is unusual in the PE world. For a portfolio company like Pediatrics Plus — which derives revenue from Medicaid, commercial insurance, and potentially TRICARE — having a PE sponsor that understands the regulatory environment from the inside is a meaningful operational advantage.

Leavitt Equity Partners’ existing portfolio includes NeuroPsychiatric Hospitals and RHA Health Services, both of which operate in behavioral health-adjacent sectors. The Pediatrics Plus investment extends the firm’s healthcare services portfolio into pediatric developmental therapy — a sector that overlaps significantly with the ABA market in terms of patient population, payer dynamics, and clinical workforce.

First Citizens Bank’s Healthcare Finance division provided the debt financing for the transaction, which was announced separately in March 2025. The involvement of a dedicated healthcare lending team in the financing structure indicates that the Pediatrics Plus deal was structured as a leveraged acquisition rather than a pure equity investment — consistent with standard PE deal mechanics in healthcare services.

The Multi-Specialty Model: Why It Matters for ABA

The ABA industry has developed largely as a single-specialty sector. The overwhelming majority of PE-backed ABA platforms offer ABA therapy as their primary or exclusive service. This specialization has advantages: it simplifies operations, allows deep clinical expertise, and creates a focused value proposition for payers. But it also creates vulnerabilities that multi-specialty providers like Pediatrics Plus do not face.

Revenue diversification: a single-specialty ABA provider generates 100 percent of its revenue from ABA-related billing codes, primarily CPT 97153 (adaptive behavior treatment by protocol), 97155 (adaptive behavior treatment with protocol modification), and 97156 (family adaptive behavior treatment guidance). If a payer cuts reimbursement for ABA codes, the revenue impact is immediate and total. A multi-specialty provider that offers ABA alongside OT, PT, and speech therapy has revenue distributed across multiple CPT code families, which provides a natural hedge against rate reductions in any single therapy category.

Clinical integration is the second advantage. Children with autism spectrum disorder frequently require not only ABA therapy but also speech therapy, occupational therapy, and sometimes physical therapy. In a single-specialty ABA model, families must coordinate these services across multiple providers, often at different locations with different schedules. In a multi-specialty model, all therapies can be delivered at the same location, coordinated by the same clinical team, and billed through the same intake and authorization process. This integration reduces family burden, improves therapy coordination, and can lead to better clinical outcomes.

Workforce economics: multi-specialty providers also benefit from workforce diversification. The ABA industry faces acute shortages of BCBAs and RBTs, and competition for these clinicians drives wage inflation that compresses margins. A provider that employs occupational therapists, speech-language pathologists, and physical therapists in addition to BCBAs and RBTs is less vulnerable to labor market disruptions in any single clinical discipline. If BCBA supply tightens, the multi-specialty provider can continue operating its OT, PT, and speech services while adjusting its ABA capacity.

The strategic implication for the ABA industry is that PE buyers may increasingly prefer multi-specialty targets over pure-play ABA providers. A multi-specialty platform offers diversified revenue, integrated clinical services, and workforce resilience — all of which reduce the risk profile of the investment and potentially support higher valuation multiples. If this preference accelerates, it could shift the competitive landscape by favoring ABA providers that have expanded into adjacent therapies over those that have remained single-specialty.

For ABA practice owners evaluating their market positioning, the Leavitt-Pediatrics Plus deal raises a direct strategic question: is the long-term competitive advantage in deepening ABA specialization, or in broadening into a multi-specialty pediatric therapy model that reduces payer risk and creates clinical integration value?

Western Governors University: An Unusual Co-Investor With a Workforce Angle

The involvement of Western Governors University as a co-investor in the Pediatrics Plus transaction is one of the most unusual elements of the deal. WGU is a nonprofit, online university that offers competency-based degree programs, including programs in healthcare. Its investment arm, Juvo Ventures, participates in the Pediatrics Plus investor group alongside Leavitt and Fulcrum.

The strategic rationale for WGU’s involvement is workforce development. Pediatric therapy providers face persistent challenges in recruiting and retaining qualified clinicians. WGU’s educational platform could serve as a talent pipeline — training future BCBAs, speech-language pathologists, occupational therapists, and physical therapists who could then be recruited into Pediatrics Plus’s clinical teams. This education-to-employment pathway, if executed effectively, would address one of the most critical bottlenecks in pediatric therapy growth: the supply of credentialed clinicians.

The WGU partnership also reflects a broader trend in healthcare PE: the recognition that workforce supply is not merely an operational challenge but a strategic asset. PE-backed healthcare platforms that can develop proprietary talent pipelines have a durable competitive advantage over platforms that compete for the same limited pool of clinicians on the open market. The Pediatrics Plus deal structure — with a university as a co-investor and workforce development partner — is an innovative approach to this problem.

For the ABA industry specifically, where BCBA supply constraints are among the most frequently cited barriers to growth, the WGU model is worth watching. If the Pediatrics Plus-WGU partnership demonstrates that education-to-employment integration can meaningfully improve clinician recruitment and retention, it could become a template for other PE-backed platforms to replicate.

AT A GLANCE

| Lead PE investor: | Leavitt Equity Partners (Salt Lake City, UT); founded 2014 by Mike Leavitt |

| Co-investors: | Fulcrum Equity Partners (Atlanta, GA); Western Governors University / Juvo Ventures |

| Target company: | Pediatrics Plus (Conway, AR); founded 2002 by Todd and Amy Denton |

| CEO: | Scott Street, Pediatrics Plus |

| Services: | ABA therapy, physical therapy, occupational therapy, speech-language pathology |

| Children served annually: | More than 6,000 |

| States of operation: | Arkansas and Texas |

| Related brands: | The Farm by Pediatrics Plus, Community Connections, Rise Counseling & Diagnostics |

| LEP AUM: | Over $400 million in capital from strategic healthcare LPs |

| Founder role post-deal: | Todd and Amy Denton remain largest shareholders; both on board |

| Financial advisor: | Stephens Inc. (exclusive advisor to Pediatrics Plus) |

| Debt financing: | First Citizens Bank Healthcare Finance (announced March 2025) |

SOURCES & REFERENCES

| 1. | Leavitt Equity Partners. “Pediatrics Plus Partners with Leavitt Equity Partners for Next Phase of Growth.” Press release via Business Wire. January 13, 2025. |

| 2. | Behavioral Health Business. “2 PE Firms, Private College Invest in Multi-Specialty Developmental Care Provider Pediatrics Plus.” January 13, 2025. |

| 3. | First Citizens Bank. “First Citizens Bank Provides Financing to Leavitt Equity Partners to Acquire Pediatrics Plus.” Press release. March 12, 2025. |

| 4. | Stephens Inc. “Pediatrics Plus” transaction page. stephens.com. January 2025. |

| 5. | CB Insights. “Leavitt Equity Partners Portfolio Investments.” Accessed April 2026. |

| 6. | Mertz Taggart. “Q1 2025 Behavioral Health M&A Report.” 2025. |