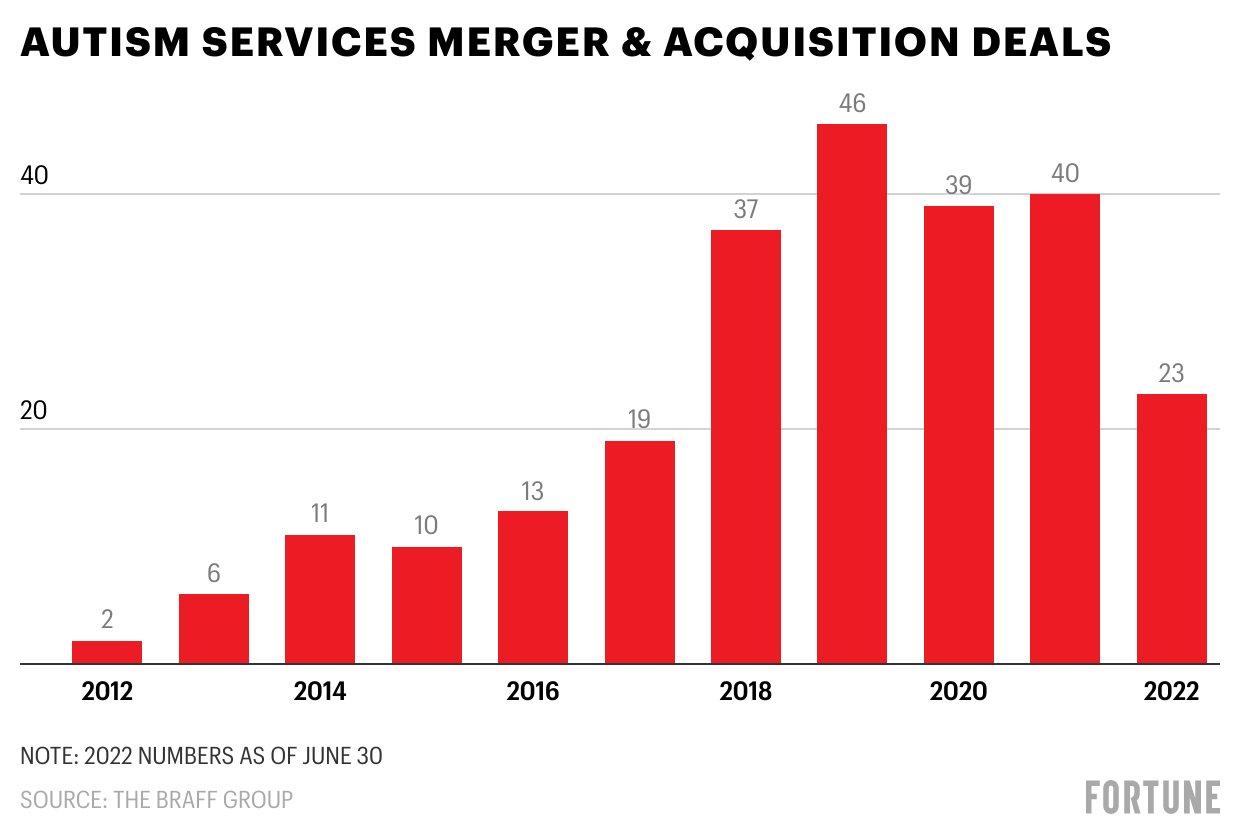

574 Centers, 42 States, 147 Deals

PROVIDENCE, R.I. — The study, published January 5 in JAMA Pediatrics by researchers at Brown University’s Center for Advancing Health Policy through Research, provides one of the first national assessments of private equity’s footprint in autism services. Using data from PitchBook, public press releases, and manually verified company websites, the research team identified 574 autism therapy centers owned by PE firms as of December 31, 2024, spanning 42 states. The study offers what its authors describe as a first step toward understanding an investment trend that has reshaped the delivery of autism services with little public scrutiny.

The acquisition timeline is concentrated and rapid. Nearly 80 percent of all PE acquisitions of autism centers occurred between 2018 and 2022, the result of 147 separate deals. The geographic concentration mirrors the industry’s revenue geography: California leads with 97 PE-owned centers, followed by Texas (81), Colorado (38), Illinois (36), and Florida (36). Sixteen states had one or zero PE-owned clinics. States in the top third for childhood autism prevalence were 24 percent more likely to have a PE-owned clinic, and investment was more common in states with fewer limits on insurance coverage—the regulatory conditions that make ABA therapy most profitable.

The timing of the PE surge is not coincidental. The acceleration from 2018 to 2022 corresponds precisely with the period in which state insurance mandates for autism services reached near-universal coverage, Medicaid behavioral health mandates took full effect, and autism prevalence data showed continued increases. PE firms recognized that the combination of mandated insurance coverage, rising prevalence, and a fragmented provider landscape created the conditions for rapid consolidation—the same conditions that drove PE investment in dental chains, dermatology practices, and emergency medicine groups in prior waves of healthcare consolidation.

Study author Yashaswini Singh, a health economist at Brown’s School of Public Health, framed the findings in terms of risk. She noted that this is yet another segment of healthcare that has emerged as potentially profitable to PE investors, and that it is very distinct from where investors have traditionally gone, making the potential for harm more serious. She added that because many of these children are insured by Medicaid, increased intensity of care by PE-owned providers translates into increased claims against taxpayer-funded programs.

Daniel Arnold, a senior research scientist at Brown and the study’s lead author, was more direct about the financial incentives at play. He expressed concern about revenue-generating strategies seen in other PE-backed healthcare settings—specifically that children might receive more services than clinically appropriate, and that disparities in access could worsen if PE firms prioritize high-revenue markets over underserved communities. The researchers did not evaluate the impact of PE ownership on care quality or outcomes in this study, but they are now seeking federal funding to examine exactly those questions.

States in the top third for childhood autism prevalence were 24 percent more likely to have a PE-owned clinic. The investment follows the insurance money—and the insurance money follows the diagnosis.

The CEPR Report: 85 Percent of All Autism M&A

The Brown study’s quantitative mapping is complemented by a comprehensive policy report from the Center for Economic and Policy Research, authored by Rosemary Batt of Cornell University and Eileen Appelbaum of CEPR. The report, titled “Pocketing Money Meant for Kids: Private Equity in Autism Services,” provides a detailed assessment of the PE business model in autism care and its consequences for workers, families, and the public programs that fund services.

The CEPR report’s central finding: between 2017 and 2022, private equity firms completed 85 percent of all mergers and acquisitions in the autism healthcare segment—a rate not found in any other segment of healthcare or any other industry. PE firms are now the dominant for-profit providers in the sector, having created massive national chains through rapid consolidation of small independent providers. The 12 PE-owned autism service chains examined in the report employ at least 30,000 people at approximately 1,300 locations, with annual estimated revenues of $5 to $7 billion.

The report identifies a consistent pattern: large generalist PE firms with little or no experience in autism services acquire providers using substantial debt, load that debt onto the provider organization, and then sell the chain to another PE firm on average every four years. Almost all PE owners in the study are large generalist firms investing across industries from fossil fuels to retail, with virtually no knowledge or experience in providing services to autistic children. Post-buyout, PE-owned chains exhibit lower levels of staffing, training, and supervision—all of which undermine both job quality and care quality.

Some PE owners prioritize patients who can garner higher billing rates or states with higher reimbursement rates, worsening inequality in access to care. Employees at PE-owned organizations report pressure to standardize treatment plans and to bill for more hours per patient than is medically necessary—leading in some instances to fraud allegations and compliance investigations. The report notes that autism services became a hot market for PE acquisitions only after widespread health insurance coverage became available by the mid-2010s, through the passage of state mandates, the ACA, and the Medicaid behavioral health mandate.

Professor Rosemary Batt of Cornell, the report’s lead author, summarized the dynamic: parents who fought for health insurance coverage for their autistic kids expected the funds to be used to expand access to high quality treatment. They did not expect private equity firms to move in, skim reimbursements to pay high salaries to executives, and deliver millions to private equity partners. The framing is pointed, but it is supported by the report’s detailed case studies of specific PE-owned chains.

Between 2017 and 2022, PE firms completed 85 percent of all mergers and acquisitions in autism services. The rate is unmatched in any other healthcare segment—or any other industry.

The Blackstone/CARD Case Study

The most dramatic illustration of PE’s impact on autism services is the Blackstone/CARD case. When Blackstone acquired the Center for Autism and Related Disorders in 2018, CARD was the largest autism services chain in the United States, with approximately 250 locations across multiple states. CARD had been founded by Dr. Doreen Granpeesheh, a clinical psychologist who built the organization over decades into the nation’s premier ABA provider.

Under Blackstone’s ownership, CARD was loaded with debt that it had not previously carried. The CEPR report documents that Blackstone began making substantial cuts to the company’s training requirements, shifting from in-person to online training and cutting the weeks of new hire orientation in half. Within five years, Blackstone had closed over 100 of CARD’s 250 locations—substantially decreasing rather than increasing access to care for the families those clinics served.

CARD entered bankruptcy in June 2023, representing one of the largest failures of a PE-backed healthcare provider in recent years. The bankruptcy left families scrambling to find alternative ABA providers, disrupted treatment continuity for hundreds of children, and eliminated jobs for thousands of clinicians and technicians. The case demonstrates the specific risk that PE’s debt-driven business model poses to service continuity in a sector serving vulnerable children—a population that depends on consistent therapeutic relationships and cannot easily absorb disruptions in care.

The ACES/Ally Pediatric Deal: A Case Study in PE Strategy

The January 2026 acquisition of Ally Pediatric Therapy by ACES provides a real-time illustration of how PE-backed consolidation reshapes service delivery. ACES, backed by General Atlantic, announced the acquisition of Ally Pediatric Therapy, a Phoenix-based provider of ABA, speech-language therapy, and occupational therapy, from SBJ Capital. The deal expanded ACES to 92 locations across Arizona, California, Colorado, Hawaii, North Carolina, Oklahoma, and Texas. For more than three decades, ACES has provided individualized, evidence-based ABA therapy.

The strategically significant element was what happened after the acquisition. ACES announced that over the coming months, Ally’s physical health services—including in-house speech, occupational therapy, and feeding services—would be replaced with external care coordination. The company framed the decision in clinical terms: focusing exclusively on ABA allows the combined company to concentrate on being the best in a single service line. Berkery Noyes served as financial advisor to Ally, with O’Melveny & Myers as legal counsel and Bass Berry & Sims for ACES.

The transition to an ABA-only model reflects a broader trend in PE-backed autism consolidation. ABA therapy commands higher reimbursement rates and authorizes more intensive hours per client than speech or occupational therapy, making it the most revenue-productive service line. By stripping allied services and focusing on ABA, PE-backed platforms maximize revenue per center while simplifying operations. The trade-off is that families receiving integrated multidisciplinary care must now coordinate across multiple providers, fragmenting the treatment experience at a time when research increasingly supports holistic, multidisciplinary approaches to autism.

The PE Stakeholder Project, which tracks private equity healthcare acquisitions, noted the deal in its January 2026 monthly report, flagging that ACES ended Ally’s multidisciplinary health services including speech, occupational therapy, and feeding services following the acquisition. The framing underscores the tension: General Atlantic’s investment thesis for ACES is that focused ABA delivery at scale generates superior returns. The clinical question—whether families are better served by integrated multidisciplinary care or by a pure-play ABA model with external referrals—is secondary to the financial logic of the platform strategy.

The Regulatory and Political Context

The Brown study’s publication in early January 2026 arrives in a political environment where autism is in the national spotlight. Autism diagnoses among U.S. children have nearly tripled between 2011 and 2022, and the condition has been the subject of intense political debate, including false claims linking autism to childhood vaccines. The CDC changed its website language in late 2025 regarding vaccine-autism consensus, further politicizing the diagnostic landscape and drawing attention from federal officials including the HHS Secretary.

The regulatory response to PE’s role in autism services remains nascent. The Brown researchers did not evaluate the impacts of PE ownership on access, quality, or family experience. The team is now seeking federal funding from the National Institute on Aging and the National Institute on Mental Health to study how PE ownership affects therapy intensity, medication use, diagnosis age, and treatment duration. Singh has noted that PE investment is not inherently harmful and that making money while expanding access is not necessarily a bad thing. But the scale and speed of consolidation warrant systematic study.

At the state level, several legislatures are grappling with related questions. Illinois is considering bills that would repeal its requirement for clinician ownership of ABA practices—a requirement that effectively restricts PE ownership structures. Other states are examining utilization controls, rate adjustments, and care quality standards that would affect PE-backed providers disproportionately because of their scale. The question of whether PE involvement in autism services expands access or extracts value from a vulnerable population is likely to be one of the defining policy debates in ABA over the next several years.

The CEPR report offers specific policy recommendations. The autism community should push for state and federal legislation to establish minimum care standards for provider organizations, including rules for minimum staff-client ratios and the mix of skills and qualifications needed to provide appropriate care. Legislation should include annual reporting requirements and monitoring and oversight that currently do not exist. These recommendations reflect the report’s central argument: the regulatory vacuum in which PE-backed autism providers operate allows financial incentives to override clinical judgment without accountability.

The data are now on the table: 574 centers, 42 states, 85 percent of all M&A, $5–7 billion in annual revenues, and a business model that loads debt, strips services, and flips ownership every four years. Whether that model serves the interests of autistic children and their families—or primarily serves the interests of the limited partners who fund the deals—is the question that the next phase of research, regulation, and political engagement will need to answer.

AT A GLANCE

| PE-owned autism centers (2024): | 574 across 42 states (Brown/JAMA Pediatrics) |

| Acquisition timeline: | ~80% acquired 2018–2022; 147 deals total |

| Top states: | CA (97), TX (81), CO (38), IL (36), FL (36) |

| PE share of autism M&A: | 85% of all deals, 2017–2022 (CEPR report) |

| CEPR report authors: | Rosemary Batt (Cornell) and Eileen Appelbaum (CEPR) |

| Annual industry revenues: | $5–$7 billion (CEPR estimate) |

| PE chains profiled: | 12 chains; 30,000+ employees; ~1,300 locations |

| ACES/Ally deal (Jan 2026): | ACES (General Atlantic) acquired Ally; transitioned to ABA-only |

| ACES post-deal locations: | 92 across AZ, CA, CO, HI, NC, OK, TX |

| Blackstone/CARD outcome: | ~250 locations reduced to ~100; bankruptcy June 2023 |

| JAMA Pediatrics DOI: | 10.1001/jamapediatrics.2025.5443 |

SOURCES & REFERENCES

| 1. | Singh, Y., Arnold, D., et al. “Private Equity in Autism Services.” JAMA Pediatrics. January 5, 2026. |

| 2. | Brown University. Press release. January 7, 2026. brown.edu. |

| 3. | U.S. News. “Autism Therapy Centers Targeted By Private Equity.” January 6, 2026. |

| 4. | Disability Scoop. “Private Equity Increasingly Taking Over Autism Therapy Centers.” February 2026. |

| 5. | Batt, R., Appelbaum, E. “Pocketing Money Meant for Kids: PE in Autism Services.” CEPR. June 2023. |

| 6. | PE Stakeholder Project. “PE Health Care Acquisitions – January 2026.” pestakeholder.org. |

| 7. | BusinessWire. “ACES Announces Acquisition of Ally Pediatric Therapy.” January 15, 2026. |

| 8. | BHB. “ACES Acquires Ally Pediatric Therapy, Transitions to ABA-Only Model.” January 16, 2026. |

| 9. | Becker’s. “Rapid private equity growth in autism care sparks scrutiny.” January 5, 2026. |

| 10. | MedicalXpress. “Private equity acquired more than 500 autism centers.” January 5, 2026. |