The Audit That Set the Standard

WASHINGTON, D.C. – On December 16, 2024, the U.S. Department of Health and Human Services Office of Inspector General issued audit report A-09-22-02002: Indiana Made at Least $56 Million in Improper Fee-for-Service Medicaid Payments for Applied Behavior Analysis Provided to Children Diagnosed With Autism. It was the first completed report in a planned seven-state federal review of Medicaid ABA billing that the OIG had announced in January 2022. The headline number — $133 million in confirmed improper and potentially improper payments over two years in a single state — was striking. The methodology behind it was more so.

The auditors examined Indiana’s fee-for-service Medicaid ABA payments for 2019 and 2020, a period during which total FFS ABA spending in Indiana was $151.1 million — $104.5 million of which was the federal share. From that universe, they drew a random sample of 100 enrollee-months from 41 unique ABA facilities and 96 unique enrollees, representing $967,294 in payments. They then applied a standard statistical extrapolation methodology to project findings across the full payment population.

The result: auditors found at least $56.6 million in confirmed improper payments and an additional $76.7 million in potentially improper payments — a combined $133.3 million. Of the improper amount, $39.4 million was the federal share, which the OIG recommended Indiana refund to the federal government. Of the potentially improper amount, $53.2 million was the federal share, which the OIG directed Indiana to review and refund to the extent improper.

The most important sentence in the report was buried in the findings summary: of the 100 sampled enrollee-months, 97 included at least one claim line that did not comply with federal and state requirements. Three out of 100 were clean. The other 97 had something wrong.

“The State agency made improper and potentially improper payments because it did not provide effective oversight of [fee-for-service] Medicaid ABA payments. Specifically, the State agency did not provide sufficient guidance to ABA facilities for documenting ABA.” — HHS-OIG Audit Report A-09-22-02002, December 2024

The Six Categories of Billing Failure

The Indiana audit identified billing deficiencies across six distinct categories. Understanding them specifically matters because they are not unique to Indiana — every subsequent state audit in the OIG series has identified the same structural problems.

1. Session notes that did not meet documentation requirements. This was the most pervasive finding and the primary driver of improper payments across all audited states. Documentation requirements for ABA CPT codes are specific: session notes must include time in and time out, names of all staff and caregivers present, place of service, the rendering provider’s signature, and — for codes like 97155 (adaptive behavior treatment with protocol modification) — specific documentation of what protocol was modified, how, and why. The auditors found that the majority of sampled session notes failed to adequately support the CPT codes billed. In many cases, data entries existed but narrative content was absent; in others, time documentation was present but did not reconcile with the number of units billed.

2. Group therapy billed as individual therapy. CPT code 97153 covers one-on-one adaptive behavior treatment by a technician. CPT code 97154 covers group adaptive behavior treatment for two or more patients simultaneously. The audits found instances in which providers billed 97153 — the individual, higher-reimbursing code — for sessions that the clinical documentation reflected were actually group sessions. This is a straightforward upcoding violation. The reimbursement difference is not trivial: individual codes reimburse at materially higher rates than group codes, per 15-minute unit.

3. Non-therapy time included in billable hours. The Indiana audit specifically cited instances in which ABA time was billed continuously without adjustment for non-billable activities including meals and bathroom breaks. As stated in the OIG report, most session notes “documented that ABA time was billed continuously without any adjustment to the units of service for potential nontherapy times, such as meals.” The same finding appeared in the Wisconsin audit. Medicaid rules require that billable ABA time reflect only direct therapeutic service. Rounding up, billing through breaks, or failing to account for non-therapy periods within a continuous session creates over-billing on every affected claim.

4. Services by staff without appropriate credentials. Indiana Medicaid ABA billing requires that each CPT code be rendered by a provider with the appropriate credential level. CPT 97155 — adaptive behavior treatment with protocol modification — can only be billed by a qualified healthcare professional such as a BCBA. CPT 97153 is typically delivered by a technician (RBT) under supervision. The audits found instances in which claims were submitted under credential levels inconsistent with who actually provided the service, or under providers who lacked documentation of the required qualifications. The Colorado audit in February 2026 went further, estimating that as many as 1,500 to 2,000 behavioral technicians in the state may have been working without the mandated 40-hour training, competency check, and required supervision.

5. Missing or invalid diagnostic evaluations and treatment referrals. Indiana Medicaid requires that children receiving ABA have a documented diagnostic evaluation confirming autism and a referral recommending ABA before services begin. The audit found instances in which these prerequisites were absent or outdated. One case cited in detail by Indiana Capital Chronicle’s coverage of the audit involved a child who had an ABA referral from 2014 but no documented follow-up to reassess medical necessity. By the summer of 2020 — six years later — the child was receiving five days a week of ABA with over seven hours of therapy per day at age eight. No updated clinical justification was on file.

6. Unsupported 97155 billing and excessive units. CPT code 97155 is among the most scrutinized codes in ABA Medicaid billing because it can be billed concurrently with 97153 when a qualified provider is actively modifying a treatment protocol during a session. Auditors found widespread use of 97155 for supervision or observation activities that did not meet the modification threshold, as well as claims in which the number of units billed exceeded what the session time could support. The Benesch law firm’s January 2026 compliance alert on the Indiana and Wisconsin audits specifically flagged “unsupported CPT code billing, including excessive units, and overlapping service times” as among the deficiencies found.

The Context: How Indiana Got Here

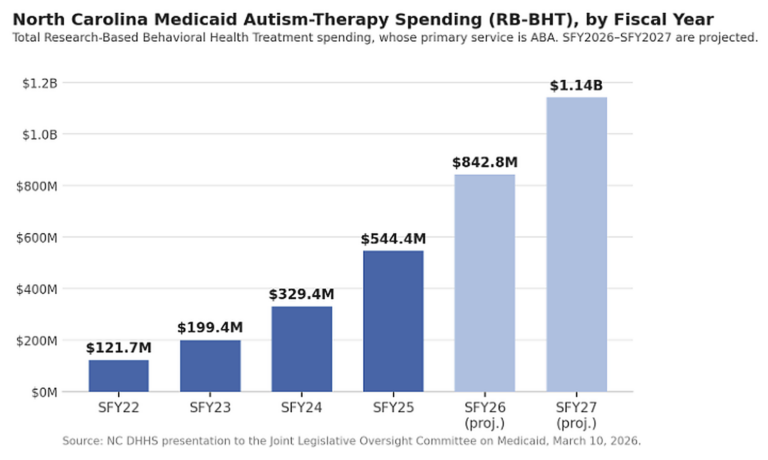

Indiana’s ABA Medicaid spending trajectory is among the most extreme in the country. FFS payments for ABA were $14.4 million in 2017. By 2020 — the last year covered by the OIG audit — they had reached $101.8 million, making Indiana second highest in the nation. By 2023, total ABA expenditures had reached $611 million, up from $21 million six years earlier — a 2,800% increase. The state’s Medicaid-enrolled individual ABA therapists grew from 797 in 2020 to 2,534 by the end of 2024.

One driver of that spending growth that the Indiana ABA advocacy community has cited explicitly: private equity-backed providers billing at rates that a fee schedule had not yet capped. According to the Behavior Associates of Indiana, before the state established a fixed fee schedule in January 2024, some providers and private equity-backed organizations charged Indiana Medicaid fees of up to $900 or more per hour. The prior system paid a percentage of billed charges without an established rate ceiling. A state that had not built oversight infrastructure for a $21 million program was suddenly administering a $600 million one.

The Indiana Family and Social Services Administration launched a fixed fee schedule in January 2024 — $55.16 per hour for RBT-delivered services and $103.77 per hour for qualified clinicians — which drove spending from $611 million (2023 peak) to $445 million in 2024. Gov. Mike Braun’s administration subsequently convened a working group to recommend further cost containment strategies and proposed a 30-hour weekly cap with a three-year lifetime limit, which was then withdrawn as politically untenable. FSSA initiated a program integrity review of all ABA claims from 2022 through 2025, the results of which will require providers to refund overpayments and complete compliance training.

“This is something that’s very valuable — but at the same time, we know it’s unsustainable, the current cost trajectory.” — Eric Miller, former Director, Indiana Department of Child Services, November 2025

The Audit Series: Every State, Same Result

The Indiana audit was the first of a planned seven-state series. Three more have been completed. In each one, every sampled claim contained at least one improper or potentially improper payment. That is not a finding of isolated fraud by a few bad actors. It is a finding of systemic documentation and billing failure across the provider ecosystem.

Wisconsin (Report A-06-23-01002, July 2025): The OIG examined Wisconsin’s FFS ABA payments for 2021 and 2022, during which total FFS ABA spending was $53.7 million annually. All 100 sampled enrollee-months contained improper or potentially improper payments. Confirmed improper: at least $18.5 million. Potentially improper: an estimated $94.3 million. The primary cause was session notes that did not support the billed CPT codes; the second most common cause was session notes that did not support the number of units billed. OIG recommended Wisconsin refund $12.3 million in federal share. Wisconsin partially concurred with the repayment recommendation and agreed to the corrective action recommendations.

Maine (Report A-01-24-00006, January 2026): Maine’s audit covered rehabilitative and community support (RCS) services — which include ABA and other evidence-based treatments for children with autism. Confirmed improper payments: at least $45.6 million. Federal share to be returned: $28.7 million. The OIG noted this was the third completed audit in the ABA series. Maine agreed with recommendations for corrective action.

Colorado (Report A-09-24-02004, February 25, 2026): Colorado’s ABA FFS spending grew from $60.1 million in 2019 to $163.5 million in 2023. The OIG reviewed $289.5 million in payments across more than one million claims for 2022 and 2023. All 100 sampled enrollee-months contained improper or potentially improper payments. Confirmed improper: at least $77.8 million. Federal share to be returned: $42.6 million. The audit flagged specific named providers and estimated that 1,500 to 2,000 behavioral technicians may have been working without required training and supervision. Colorado disagreed with the repayment recommendation, arguing that auditors had not provided claim-level documentation sufficient to support the $42.6 million figure. Three more state audits in the series remain in progress as of March 2026.

Across the four completed audits, the OIG has identified a combined confirmed improper payment total of approximately $198.5 million ($56.6M + $18.5M + $45.6M + $77.8M), with hundreds of millions more in potentially improper payments still under review. A February 2026 New York Post analysis citing multiple OIG audits characterized the combined figure as potentially reaching $600 million in improper or questionable payments across the audited states.

State and Federal Enforcement Beyond the Audits

The OIG audit series is proceeding alongside a parallel track of criminal and civil enforcement by state attorneys general and federal prosecutors. In June 2025, the Massachusetts Attorney General’s Office indicted a Medicaid-enrolled autism service provider that allegedly fabricated documentation to support more than $1 million in false claims for ABA services that were never provided. In March 2024, the Massachusetts IG had separately published a report finding up to $17.3 million in ABA overpayments in that state, citing inadequate supervision ratios, impossible billing, and holiday claims.

In Minnesota, federal prosecutors have been pursuing a series of ABA Medicaid fraud cases centered on providers in the Minneapolis Somali community. In September 2025, Asha Farhan Hassan and Abdinajib Hassan Yussuf both pleaded guilty to an autism fraud scheme. Hassan owned Smart Therapy Center and was found to have hired unqualified staff, paid kickbacks of $300 to $1,500 per month to parents to recruit children — some not diagnosed with autism — billed for services not provided, and submitted false documentation between 2019 and 2024. Minnesota had 85 open investigations into ABA providers as of the summer of 2025, following FBI raids on multiple providers in 2024.

Kevin Lownds, Division Chief at the Medicaid Fraud Control Unit for the Massachusetts Attorney General’s Office, stated publicly at the American Health Lawyers Association’s Fraud and Compliance Forum that ABA therapy was a behavioral health area where fraud and abuse was rampant, and that his unit was frequently seeing fraud warranting criminal charges — most commonly, billing for services never provided to patients. Morgan Lewis’s November 2025 Health Law Scan characterized the OIG audit activity and state enforcement as a compounding signal: ABA has been formally identified as a Medicaid fraud risk area, and both federal and state investigators are treating it as a priority.

What This Means for Compliant Providers

The enforcement landscape creates direct operational risk for ABA providers who believe their billing is accurate. The OIG audit methodology uses statistical extrapolation from a random sample — meaning a provider organization does not need to have engaged in intentional fraud to receive a repayment demand. Documentation deficiencies that are widespread in the industry — incomplete session notes, missing signatures, inadequate justification for 97155 usage, failure to document non-therapy time — are exactly the triggers that OIG sampling identifies. A provider with 1,000 clients whose session notes have even minor systematic deficiencies can face a projected overpayment calculation that dwarfs the actual billing error.

The compliance steps the OIG has recommended to every audited state are consistent and instructive for providers. They amount to four categories: (1) adequate and specific session note documentation for every billed CPT code, including narrative content and reconciled time accounting; (2) credential verification for rendering providers before each claim is submitted; (3) confirmation of active diagnostic evaluation and ABA referral on file before services begin; and (4) periodic internal postpayment review — before a federal auditor conducts one instead.

The broader question for the industry is whether the billing failures documented across Indiana, Wisconsin, Maine, and Colorado represent intentional fraud, negligent compliance, or the predictable output of a system that scaled dramatically without building the documentation infrastructure the scale required. The answer is almost certainly all three, distributed unevenly across the provider ecosystem. For the federal government, the distinction matters less than it might in criminal proceedings: audit-identified overpayments carry repayment obligations regardless of intent. The compliance and legal exposure created by the OIG audit series is structural, ongoing, and expanding.

AT A GLANCE

OIG Audit Series: Announced January 2022; seven-state series of fee-for-service Medicaid ABA audits; four completed as of March 2026

Indiana findings: $56.6M confirmed improper + $76.7M potentially improper = $133.3M total (2019–2020 FFS payments). 97 of 100 sampled enrollee-months had at least one improper claim line. Federal share repayment recommended: $39.4M

Audit scope (Indiana): $151.1M total FFS ABA payments examined (2019–2020); 100 enrollee-months sampled from 41 facilities, 96 enrollees; $967,294 in sampled claims

Six billing violations: (1) Inadequate session notes; (2) Group billed as individual (97154 as 97153); (3) Non-therapy time in billable hours; (4) Unqualified staff; (5) Missing diagnostic evaluations/referrals; (6) Excessive 97155 units or unsupported usage

Indiana spending arc: $14.4M (2017) → $101.8M (2020, 2nd in nation) → $611M (2023 peak) → $445M (2024, post rate schedule). >900% increase in 6 years.

Other audits (4-state total): Wisconsin: $18.5M improper, refund $12.3M (July 2025). Maine: $45.6M improper, refund $28.7M (Jan 2026). Colorado: $77.8M improper, refund $42.6M (Feb 2026). 100/100 enrollee-months with issues in all four states.

Combined confirmed (4 states): ~$198.5M in confirmed improper payments; hundreds of millions more in potentially improper; 3 more state audits in progress

Key legal standard: Repayment obligation attaches to documentation deficiencies regardless of provider intent; OIG uses statistical extrapolation from random sample to project full population overpayment

Enforcement parallel track: MA AG indictment June 2025 ($1M+ ABA fraud); Minnesota: 85 open investigations, FBI raids 2024, guilty pleas Sept 2025; Massachusetts IG report $17.3M overpayments

Indiana corrective actions: Fixed fee schedule (Jan 2024); program integrity review of 2022–2025 claims; providers required to refund overpayments and complete compliance training

Colorado dispute: Colorado disagreed with $42.6M repayment recommendation, citing lack of claim-level documentation; agreed with corrective action recommendations

OIG report citations: Indiana: A-09-22-02002 (Dec 16, 2024). Wisconsin: A-06-23-01002 (Jul 10, 2025). Maine: A-01-24-00006 (Jan 16, 2026). Colorado: A-09-24-02004 (Feb 25, 2026).

SOURCES & REFERENCES

1. – HHS-OIG. Indiana Made at Least $56 Million in Improper Fee-for-Service Medicaid Payments for Applied Behavior Analysis. Report A-09-22-02002. December 16, 2024. oig.hhs.gov

2. – HHS-OIG. Wisconsin Made at Least $18.5 Million in Improper Fee-for-Service Medicaid Payments for Applied Behavior Analysis. Report A-06-23-01002. July 10, 2025. oig.hhs.gov

3. – HHS-OIG. Maine Made at Least $45.6 Million in Improper Medicaid Payments for Autism Services. Report A-01-24-00006. January 16, 2026. oig.hhs.gov

4. – HHS-OIG. Colorado Made at Least $77.8 Million in Improper Fee-for-Service Medicaid Payments for Applied Behavior Analysis. Report A-09-24-02004. February 25, 2026. oig.hhs.gov

5. – HHS-OIG. Audits of Medicaid Applied Behavior Analysis for Children Diagnosed With Autism. Series SRS-A-25-029. Work Plan overview. oig.hhs.gov

6. – STAT News / Bannow T. Indiana Medicaid Audit Finds Questionable Payments for ABA Autism Therapy. December 19, 2024. statnews.com

7. – STAT News / Bannow T. Federal Medicaid Audit Finds Massive Overpayment for Autism Therapy in Colorado. March 2, 2026. statnews.com

8. – Behavioral Health Business. ABA Providers Improperly Billed Medicaid for $56M, Audit Reveals. December 19, 2024. bhbusiness.com

9. – Indiana Capital Chronicle. Governor’s Group Recommends ABA Usage Cap, Rate Changes as Medicaid Costs Rise. November 12, 2025.

10. – Indiana Capital Chronicle. ABA and the Medicaid Budget — What’s Next for Therapy for Children with Autism. January 13, 2025.

11. – Stateline. Families Worry as Cost of Autism Therapy Comes Under State Scrutiny. November 25, 2025.

12. – Behavior Associates of Indiana. Indiana Medicaid Proposed ABA Cuts. behavioraba.com (February 2025). PE billing $900+/hour cited.

13. – Behavioral Health Business. ABA Providers Struggle to Care for Medicaid Patients Amid Rate Stagnation, Cuts. August 28, 2023.

14. – Morgan Lewis Health Law Scan. Applied Behavioral Analysis: Key Service for Children with Autism Is Under Payment Scrutiny. November 14, 2025.

15. – Benesch. OIG Finds Significant Improper Medicaid Payments for ABA Services in Wisconsin and Indiana. beneschlaw.com. January 9, 2026.

16. – The Colorado Sun / Brown J. Colorado Wrongly Spent $78M on Autism Therapy, OIG Says. March 2, 2026.

17. – Michigan Healthcare Freedom Forum. HHS-OIG Audits Indiana & Wisconsin Autism Programs. mihealthfreedom.org (February 2026). Cites New York Post, March 3, 2026.

18. – Massachusetts Attorney General’s Office. Indictment of ABA Provider for >$1M in False Claims. June 2025.

19. – U.S. Department of Justice. Minnesota ABA Fraud Guilty Pleas. September 2025. (Hassan/Yussuf, Smart Therapy Center.)

20. – BreakingNewsABA.com — March 2026