The 2024 MHPAEA Final Rule: What It Required, and Why ABA Was Central

WASHINGTON, D.C. — the Mental Health Parity and Addiction Equity Act was enacted in 2008 and has been implemented through multiple rounds of regulatory guidance, each more specific than the last. The most significant regulatory step in the law’s history was a final rule published by the Biden administration in September 2024. The 2024 final rule represented the most detailed and enforceable parity standard the law had ever had. Its core requirement was that group health plans and health insurance issuers conduct and document “comparative analyses” of the non-quantitative treatment limitations they apply to mental health and behavioral health benefits compared to medical and surgical benefits. That documentation requirement was the operational heart of the rule — and the Trump administration’s pause eliminates it.

Non-quantitative treatment limitations, or NQTLs, are the primary mechanism through which insurers have historically imposed greater restrictions on mental health and behavioral health services than on medical care. Prior authorization requirements that apply to behavioral health but not to medical services, network adequacy standards that are lower for behavioral health than for medical care, and reimbursement rates that are structurally lower for behavioral health providers — these are NQTLs, and they are the reason that a patient can often access physical therapy without prior authorization but cannot access ABA therapy without a multi-step approval process involving clinical criteria that are applied nowhere else in the same plan.

ABA therapy was specifically identified as a parity focus area in the 2024 final rule’s regulatory preamble and in CMS’s accompanying guidance. The identification of ABA as a focus area reflected the extensive documented evidence of ABA-specific parity violations: prior authorization denial rates for ABA that are substantially higher than denial rates for comparable physical health services, session limits for ABA that would not be tolerated for medical therapies of equivalent clinical necessity, and network adequacy failures for ABA providers that have produced de facto access barriers even in markets with technically compliant network rosters. The rule was designed to force insurers to make those disparities visible through the comparative analysis documentation requirement — and to create legal liability for plans that could not justify them.

What the rule required specifically: the 2024 final rule required plans to document that each NQTL applicable to behavioral health benefits was no more restrictive than the predominant NQTL applied to comparable medical and surgical benefits in the same classification. For ABA, this meant documenting that prior authorization requirements, session limits, and medical necessity criteria applied to ABA were no more restrictive than the requirements applied to comparable physical health services such as physical therapy, occupational therapy, or skilled nursing. The documentation was required to be available on request to plan participants and to federal regulators. Plans that could not produce the documentation were presumptively noncompliant.

The comparative analysis requirement represented a fundamental shift in the burden of proof in parity enforcement. Before the 2024 rule, the burden was effectively on families and providers to identify specific parity violations and bring complaints. After the 2024 rule, the burden shifted to plans and insurers to document their compliance proactively. The Trump administration’s pause reverses that shift — moving the burden back to families and providers, and removing the federal enforcement infrastructure that would have processed complaints from those who identified violations.

The 2024 MHPAEA final rule required insurers to prove parity, not just assert it. The Trump administration’s pause means insurers no longer have to document their comparative analyses at the federal level. The burden of proof has shifted back to patients and providers — who have the least information and the least resources to pursue it.

The Pause: What the Trump Administration Did and What Remains

The Trump administration paused enforcement of the 2024 MHPAEA final rule, according to analysis by the Commonwealth Fund published in 2026. The pause does not eliminate the MHPAEA statute itself, which remains in effect and prohibits group health plans from imposing more restrictive limitations on mental health and behavioral health benefits than on medical and surgical benefits. What the pause eliminates is the specific documentation, comparative analysis, and federal enforcement framework that the 2024 rule created to operationalize that prohibition.

The distinction between the statute and the implementing rule matters for understanding what legal rights remain. The underlying legal right to parity coverage exists and is enforceable through private litigation under ERISA and through state insurance department enforcement for fully-insured plans. What has been suspended is the regulatory enforcement mechanism — the CMS and DOL audit authority that the 2024 rule enhanced, the documentation requirements that made compliance visible to regulators, and the specific enforcement timelines that the rule established. Without those mechanisms, the underlying statutory right becomes a right that is difficult and expensive to exercise in practice.

For ABA therapy specifically, the pause means that commercial insurers and employer health plans that were in the process of conducting comparative analyses to comply with the 2024 rule’s requirements are no longer under federal pressure to complete that process. The prior authorization requirements, session limits, and reimbursement rate differentials that the 2024 rule was designed to eliminate can continue without the federal comparative analysis documentation requirement that would have made them legally vulnerable. Insurers who were anticipating that the rule would require them to justify their ABA-specific NQTLs are now operating without that requirement, with the consequence falling on the families and children whose access is limited by those NQTLs.

What the pause means for ABA providers: ABA providers who have been documenting parity violations as part of a strategy to use the 2024 rule’s enforcement mechanisms should understand that those mechanisms are suspended, not eliminated. The documentation of parity violations — specific prior authorization denial rates, session limit applications, comparison of ABA requirements to physical therapy requirements in the same plan — remains relevant for state insurance department complaints, private ERISA litigation, and the eventual restoration of federal enforcement. Providers who stop documenting violation patterns because the federal rule is paused are losing the evidentiary foundation for the enforcement actions that will be available when the regulatory environment changes.

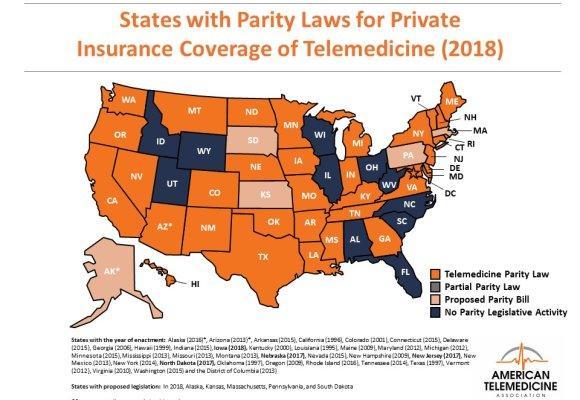

State telemedicine parity laws illustrate the geographic variation in state-level insurance regulation that applies equally to behavioral health parity. States with strong independent parity laws provide meaningful protection for fully-insured plan enrollees; states without them do not. With federal enforcement paused, state law is the only protection available for fully-insured plan enrollees — and self-funded employer plan enrollees have no state enforcement protection regardless of their state. Source: American Telemedicine Association (2018).

States as Sole Enforcers: A Patchwork With Dangerous Gaps

With federal enforcement paused, states are now the sole enforcers of mental health parity for the plans they regulate. The scope of state regulatory authority is limited in ways that most families and providers do not fully understand, and that limitation is the source of the most dangerous gap in the current enforcement landscape.

States regulate fully-insured individual and group health insurance plans issued within their borders. A fully-insured plan is one in which the insurance company bears the financial risk of claims — the employer pays premiums to the insurance company, and the insurance company pays claims. Approximately 39 percent of Americans with employer-sponsored health insurance are enrolled in fully-insured plans. For those enrollees, state parity enforcement is now the only protection available.

Self-funded employer plans are a different legal structure. In a self-funded plan, the employer bears the financial risk of claims — the employer pays claims directly from its own funds, typically with a stop-loss insurance policy to limit catastrophic exposure. Self-funded plans are governed by ERISA, the federal Employee Retirement Income Security Act, rather than by state insurance law. Under the McCarran-Ferguson Act and the ERISA preemption provisions, states cannot regulate self-funded employer plans. That means state parity enforcement authority does not apply to them regardless of how strong the state’s independent parity law is. Approximately 61 percent of Americans with employer-sponsored health insurance are enrolled in self-funded plans, according to the Kaiser Family Foundation’s employer health benefits survey. For those enrollees, the federal enforcement pause leaves them without any active parity enforcement mechanism.

The self-funded gap in practice: a family enrolled in a large employer’s self-funded health plan — which describes the majority of employees at companies with more than 200 employees — whose ABA coverage is subject to prior authorization requirements that are more restrictive than the requirements applied to comparable physical health services has a legal right to parity under MHPAEA. What they do not have is an accessible enforcement mechanism. They cannot file a complaint with the state insurance department, because the state department has no jurisdiction over their plan. They can file a complaint with the Department of Labor’s Employee Benefits Security Administration, which retains enforcement authority over ERISA plans independent of the 2024 rule pause — but EBSA enforcement is resource-constrained and individual complaint resolution can be slow. Their most accessible remedy is private ERISA litigation, which requires legal representation that most families cannot afford.

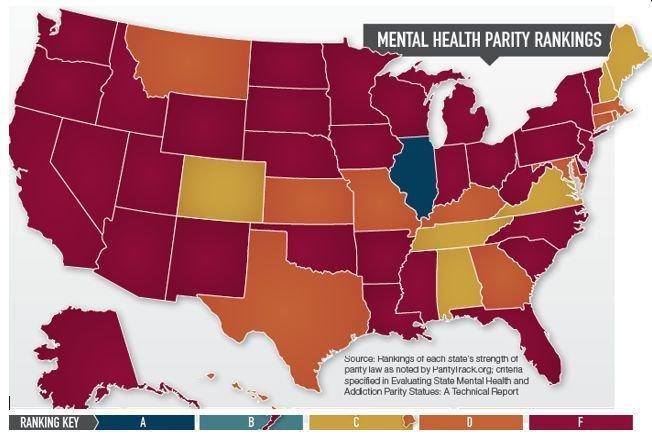

For the approximately 39 percent of employer plan enrollees in fully-insured plans, plus individuals in ACA marketplace plans and small group plans subject to state regulation, state parity enforcement is now the only protection available. Becker’s Behavioral Health’s March 2026 analysis identifies several states that have enacted parity laws stronger than the federal baseline: California, New York, Massachusetts, and Illinois are among the states with the most robust independent parity enforcement infrastructure and the most active state insurance department enforcement programs. States with weaker independent parity laws or limited insurance department enforcement capacity provide substantially less protection. The parity rankings map shown above illustrates how dramatically state-level protections vary — with the majority of states ranked D or F on ParityTrack.org’s scale.

The specific implications for ABA coverage rights depend on the state, the plan type, and the specific NQTL at issue. A family in California whose insurer is applying a prior authorization requirement for ABA that exceeds the requirement applied to comparable physical therapy has recourse through California’s independent parity enforcement framework and through California’s insurance commissioner. A family in a state with weak independent parity laws, enrolled in a self-funded employer plan, has the underlying statutory right to parity under MHPAEA but practical recourse only through EBSA complaint or private ERISA litigation.

NQTLs in Practice: What ABA-Specific Parity Violations Look Like

Understanding how NQTLs manifest specifically for ABA is essential for providers and families who want to identify potential parity violations and determine whether enforcement action is available. ABA-specific NQTLs take several distinct forms, and each form requires a different kind of comparative analysis to establish the parity violation.

Prior authorization requirements for ABA are the most common and most documented form of ABA-specific NQTL. A plan that requires prior authorization for ABA therapy sessions but does not require prior authorization for physical therapy sessions of equivalent frequency and duration is applying a more restrictive NQTL to behavioral health than to medical care. The prior authorization process for ABA often includes clinical criteria — specific diagnostic requirements, minimum behavioral assessment standards, required treatment plan formats — that go beyond what the plan applies to physical therapy. Each of those additional requirements is a potential NQTL. Documenting the specific prior authorization requirements for ABA and comparing them to the specific requirements for physical therapy in the same plan is the first step in identifying prior authorization NQTLs.

Session limits and visit caps are a second common form of ABA-specific NQTL. A plan that imposes a maximum number of ABA sessions per year, or a maximum number of hours per month, that it does not impose on physical therapy or occupational therapy is applying a quantitative treatment limitation that is more restrictive for behavioral health than for medical care. The 2008 MHPAEA statute prohibits quantitative treatment limitations that are more restrictive for behavioral health, and this prohibition remains in effect regardless of the 2024 rule pause. Families and providers who identify session limits on ABA that have no equivalent in the plan’s physical therapy coverage have a potential MHPAEA claim under the original 2008 statute.

Reimbursement rate differentials: one of the least visible but most consequential forms of ABA-specific NQTL is reimbursement rates that are structurally lower for ABA providers than for comparable medical providers in the same plan network. When ABA providers are reimbursed at rates that are not sufficient to sustain viable practices — while physical therapy providers in the same network are reimbursed at rates that are sufficient — the network becomes functionally unavailable for ABA even if it is technically populated with ABA providers. This is the mechanism that produces the “ghost network” problem in ABA: providers are listed in the network directory but are not accepting new patients because the reimbursement rate does not cover their costs. The 2024 final rule was specifically designed to address reimbursement rate NQTLs; its pause leaves that mechanism without federal enforcement.

What Providers and Advocates Can Do in the Enforcement Vacuum

The pause of the 2024 MHPAEA final rule does not eliminate legal rights; it eliminates the most accessible enforcement pathway. Families and ABA providers experiencing what they believe are parity violations have several enforcement pathways available depending on their state and plan type, and the strategic choice among those pathways requires understanding the scope and limitations of each.

State insurance department complaints are the first line of enforcement for fully-insured plans in states with independent parity enforcement authority. Many state insurance departments have specific behavioral health parity complaint processes, and several — California, New York, Massachusetts, Illinois — have dedicated behavioral health parity enforcement units that are actively pursuing complaints. A well-documented complaint that identifies the specific prior authorization requirement applied to ABA, the comparable medical service for which that requirement is not applied, the source of the comparison (the plan’s Summary Plan Description and Evidence of Coverage documents), and the specific ABA services that were denied or limited as a result is more likely to produce a substantive enforcement response than a general assertion of unfair treatment.

For self-funded employer plans covered by ERISA, the Department of Labor’s Employee Benefits Security Administration retains authority to conduct parity compliance audits independent of the 2024 final rule pause. EBSA has not announced a parallel pause of its enforcement authority over self-funded plans, and ERISA plan participants can file complaints with EBSA when they believe their employer plan is violating MHPAEA. The practical limitation is that EBSA enforcement is resource-constrained. Families and advocates should document parity violation patterns across multiple patients when possible, as aggregate evidence — showing that a specific insurer or plan is consistently applying more restrictive prior authorization requirements for ABA than for comparable physical health services — is more likely to trigger EBSA enforcement attention than isolated individual complaints.

Provider advocacy leverage: ABA providers have an advocacy role in the parity enforcement landscape that is distinct from the role of individual families. Providers who systematically track prior authorization denial rates for ABA and compare them to denial rates for physical therapy in the same plans are generating aggregate data that supports enforcement complaints, legislative advocacy, and media coverage. Organizations like the Association for Behavior Analysis International and state ABA professional organizations are positioned to aggregate provider-generated data and present it to state insurance departments, EBSA, and Congressional oversight committees as evidence of systemic noncompliance. The enforcement vacuum created by the 2024 rule pause is also a political opening for advocacy that documents the access consequences of that pause in specific states for specific patient populations.

Litigation is the most powerful but most resource-intensive enforcement pathway available to individual families in the current enforcement vacuum. Several law firms have developed ABA-specific ERISA and MHPAEA litigation practices, and some are accepting cases on a contingency basis when the denial pattern is clearly documented and the damages are substantial. Families who have experienced ABA denial or limitation that they believe reflects a parity violation and who have exhausted the insurer’s internal appeal process should consult with an ERISA benefits attorney. The internal appeal exhaustion requirement is a prerequisite for ERISA litigation, and families who skip the appeal process to pursue litigation directly may lose their legal rights.

AT A GLANCE

| 2024 MHPAEA final rule: | Required plans to document comparative analyses of NQTLs; ABA specifically identified as parity focus area |

| Trump administration action: | Paused enforcement of the 2024 final rule (Commonwealth Fund, 2026); statute itself remains in effect |

| Burden of proof shift: | Rule placed burden on insurers to document compliance; pause shifts burden back to families and providers |

| Self-funded plan gap: | ~61% of employer plan enrollees in self-funded plans; state parity law does not apply; EBSA is sole enforcement avenue |

| Fully-insured plan enforcement: | State insurance departments are sole enforcers; protection depends entirely on state law strength |

| Strong state parity enforcers: | California, New York, Massachusetts, Illinois — active enforcement units and independent parity laws |

| Weak state enforcement risk: | Majority of states ranked D or F (ParityTrack.org); limited independent enforcement infrastructure |

| ABA NQTL examples: | Prior authorization requirements stricter than physical therapy; session limits without medical equivalents; reimbursement rate differentials producing ghost networks |

| EBSA enforcement: | Retains authority over self-funded plans independent of 2024 rule pause; complaint-driven and resource-constrained |

| Provider advocacy role: | Track and aggregate denial data by insurer and service type; present to state regulators, EBSA, and Congressional oversight as systemic evidence |

| Family enforcement pathway: | State insurance complaint (fully-insured); EBSA complaint (self-funded); ERISA litigation after exhausting internal appeals |

SOURCES & REFERENCES

| 1. | Commonwealth Fund. “Behavioral Health Parity Takes a Step Backward Under Trump Administration.” 2026. commonwealthfund.org/blog/2026/behavioral-health-parity-takes-step-backward-under-trump-administration |

| 2. | Becker’s Behavioral Health. “States shaping behavioral health parity enforcement: 7 things to know.” March 2026. beckershospitalreview.com |

| 3. | Mental Health Parity and Addiction Equity Act, 29 U.S.C. § 1185a (statutory basis; remains in effect) |

| 4. | Department of Labor, Employee Benefits Security Administration. MHPAEA compliance resources. dol.gov/agencies/ebsa |

| 5. | Kaiser Family Foundation. “2023 Employer Health Benefits Survey.” kff.org (61% self-funded employer plan enrollment statistic) |

| 6. | Centers for Medicare & Medicaid Services. Final Rule: MHPAEA Implementation. September 2024. federalregister.gov (ABA as parity focus area; comparative analysis requirement) |

| 7. | ParityTrack.org. State mental health parity law rankings. paritytrack.org (parity map source data; grading methodology) |

| 8. | Employee Retirement Income Security Act, 29 U.S.C. § 1001 et seq. (ERISA preemption and self-funded plan regulatory framework) |