The Numbers Tell the Story

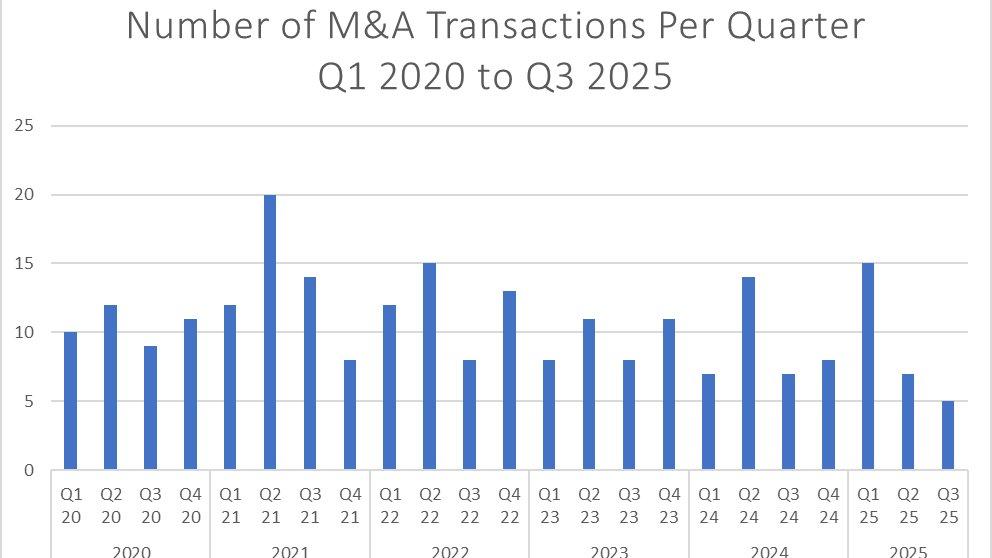

The data is unambiguous. Mertz Taggart’s Q1 2025 Behavioral Health M&A Report counted 12 transactions in the I/DD and autism subsector — the most for any quarter since the 2021 peak, when the sector reached a record 267 total behavioral health deals according to Braff Group tracking. The broader behavioral health market saw 47 total transactions, including 34 M&A deals, the most since Q4 2022. The Braff Group’s independent tracking showed an even more dramatic rebound: 14 autism/I/DD deals, representing a 133 percent year-over-year increase and a 180 percent increase from Q1 2023.

Kevin Taggart, managing partner at Mertz Taggart, provided essential context for the rebound. During COVID and right after COVID, a lot of ABA companies experienced wage inflation without getting rate increases, so there was some high-profile bankruptcy with some large providers that left California, Colorado, and other states, he said in the firm’s quarterly report. The dust has seemed to settle on that over the last six months or so, and now we’re seeing a lot of groups asking for ABA businesses. That’s a positive.

The competitive tension around deals was also notable. One ABA company that Mertz Taggart was working with in Q1 received the highest number of offers for any deal the firm had worked on since 2021. The data point is significant because it measures not just deal volume but buyer appetite: multiple bidders competing for the same target indicates that PE sponsors and strategic acquirers view the current market as an entry point with favorable risk-reward dynamics.

BHB reported that data provided by The Braff Group show dealmaking was up by 133 percent at 14 deals compared to the same period in 2024 and up 180 percent compared to the first quarter of 2023. Mertz Taggart’s data showed 12 deals in the first quarter, a year-over-year increase of 71 percent and a 140 percent increase compared to the first quarter of 2023. The fact that two independent tracking sources both report dramatic increases provides triangulation that the rebound is real rather than an artifact of a single firm’s deal flow.

During COVID and right after, a lot of ABA companies experienced wage inflation without getting rate increases, leading to high-profile bankruptcies. The dust has seemed to settle, and now we’re seeing a lot of groups asking for ABA businesses. That’s a positive. — Kevin Taggart, Managing Partner, Mertz Taggart

The 12 Transactions

Mertz Taggart’s Q1 2025 report documented the following transactions in the I/DD and autism subsector. Ascend Capital Partners, a healthcare-focused PE firm, acquired a majority stake in Unison Therapy Services, a Walnut Creek, California–based multi-specialty youth and family behavioral health provider. The deal brought a New York City–based PE firm into the California ABA market, signaling that investor interest extends beyond the Southeast and Texas markets that have dominated recent deal flow.

Leavitt Equity Partners partnered with Pediatrics Plus in Conway, Arkansas, in a deal that also involved Fulcrum Equity Partners and Western Governors University. The involvement of a university in an ABA investment is unusual and reflects the workforce development thesis: the industry’s BCBA shortage may be addressable through academic partnerships that create pipelines of trained clinicians.

BrightSpring Health Services divested its I/DD division to Sevita, formerly known as The Mentor Network, in a deal valued at $835 million. The transaction was the largest single deal in the quarter by disclosed value and represented a portfolio rationalization by BrightSpring rather than a growth acquisition. Sevita, one of the largest I/DD service providers in the country, expanded its scale through the deal.

Already Autism Health completed its two acquisitions: Commonwealth ABA in Kentucky (adding locations in GA, KY, IN, VA) and C.A.B.S. Autism & Behaviour Specialists in Illinois and Georgia, both backed by Triton Pacific Healthcare Partners. The coordinated deal execution — PE investment plus two tuck-ins announced in the same week — exemplified the platform-building model.

Regency ABA, a Georgia-based provider, acquired Magnolia Behavior Therapy in Seattle, Washington, in a cross-country deal that brought a Southeast operator into the Pacific Northwest. Strawberry Fields, a not-for-profit provider, became an affiliate of Devereux Advanced Behavioral Health, one of the oldest and largest behavioral health organizations in the country. Delta Behavioral Health Group was acquired by SpringHealth Behavioral Health & Integrated Care.

Frontera Health, an autism services startup backed by AI technology, raised $32 million in a seed funding round led by Lux Capital and Lightspeed Venture Partners. While technically a venture capital deal rather than an M&A transaction, the Frontera raise signals investor belief that AI-powered autism services represent the next frontier of the sector’s evolution. The $32 million seed round was one of the largest in ABA/autism services history.

Why the Rebound Is Happening Now

The ABA M&A rebound is driven by the convergence of several factors that have shifted from headwinds to tailwinds. First, the wage inflation that compressed margins in 2022–2024 has moderated. RBT and BCBA compensation levels have stabilized in most markets, and providers that survived the wage shock have adjusted their operating models accordingly. The survivors are leaner, more efficient, and more attractive as acquisition targets than they were during the inflationary period.

Second, the high-profile bankruptcies and market exits that shook investor confidence have been absorbed by the market. Providers that left California, Colorado, and other states created market vacuums that remaining operators are filling. The exits reduced competitive density in some markets, improving the unit economics for the operators that stayed.

Third, autism diagnosis rates continue to rise. The CDC’s 2025 report found that 1 in 31 children is now diagnosed with ASD, up from 1 in 36. The demand for ABA services shows no signs of decelerating, and the supply of providers — while growing — has not kept pace. This fundamental supply-demand imbalance makes ABA an attractive sector for investors with a multi-year time horizon.

Fourth, interest rates, while still elevated relative to the near-zero rates of 2020–2021, have stabilized and begun to decline. Lower borrowing costs improve the economics of leveraged acquisitions and make deal financing more accessible. PE firms with significant undeployed capital — dry powder — are under pressure from their limited partners to put that capital to work, creating buyer demand that supports deal volume.

Fifth, and perhaps counterintuitively, the regulatory enforcement environment may be contributing to deal activity rather than suppressing it. The OIG audits, the Wall Street Journal investigation, and state-level reforms are creating distressed acquisition opportunities and eliminating weak competitors. PE sponsors with compliance expertise see the regulatory correction as a buying opportunity: acquire compliant operators at favorable valuations while non-compliant competitors face enforcement actions, rate cuts, and payer contract terminations.

What the Rebound Means for Practice Owners and Investors

For ABA practice owners considering a sale, the Q1 2025 data provides the most concrete evidence since 2021 that the buyer market is active and competitive. Multiple dealmakers told BHB that more tailwinds than headwinds exist for behavioral health transactions. Dan Davidson of Northborne Partners noted robust interest across autism, substance use, and virtual care. Alex Veach of Agenda Health said the underlying demand for services is predominant and only trending in one direction. Peter Lynch of Stoneridge Partners observed that deals may be smaller and quieter, but there is plenty of activity out there.

The competitive dynamics of Q1 2025 suggest that well-prepared sellers with strong clinical outcomes, clean documentation, verified credentials, and diversified payer mixes can command significant buyer interest. Taggart’s observation that one deal received the highest number of offers since 2021 indicates that the best assets are attracting premium attention. For sellers, this means that investing in compliance and clinical quality before going to market is not just a regulatory necessity but a valuation driver.

For PE sponsors evaluating the ABA sector, the data confirms that the thesis remains viable despite the regulatory headwinds. The key underwriting question has shifted from whether ABA is a good investment category to which ABA operators can demonstrate the compliance rigor and clinical quality that the new enforcement environment demands. The sponsors that can distinguish between compliant and non-compliant targets — and that build compliance infrastructure into their platform investments — will be the ones that generate returns in the current environment.

For the ABA industry as a whole, the Q1 2025 rebound marks the beginning of what many expect to be a sustained period of consolidation. The 2021 peak of 267 behavioral health deals was followed by a correction. The 2025 rebound represents a market that has absorbed the correction���s lessons and is building again on a more sustainable foundation. Whether that foundation proves truly sustainable — or whether it produces another cycle of overexpansion and correction — will depend on whether the deals being made today are built on clinical quality and compliance or merely on financial engineering and geographic ambition.

AT A GLANCE

| Mertz Taggart Q1 2025: | 12 I/DD/autism transactions; highest since Q2 2021; 47 total BH deals; 34 M&A |

| Braff Group Q1 2025: | 14 autism/I/DD deals; +133% YoY; +180% vs Q1 2023 |

| Largest Q1 deal: | BrightSpring I/DD division to Sevita ($835M) |

| Notable deals: | Ascend/Unison; Leavitt/Pediatrics Plus; Already Autism/Commonwealth+CABS; Frontera $32M seed |

| Buyer appetite: | One ABA deal received highest number of offers since 2021 (Mertz Taggart) |

| Rebound drivers: | Wage stabilization, bankruptcy absorption, rising diagnosis rates, lower interest rates, enforcement-driven distress |

| Expert outlook: | “More tailwinds than headwinds” — multiple dealmakers cited by BHB |

SOURCES & REFERENCES

| 1. | Mertz Taggart. “Q1 2025 Behavioral Health M&A Report.” mertztaggart.com. |

| 2. | BHB. “Alongside, ABA Unlimited Announce Deals As M&A Pops in 2025.” May 27, 2025. |

| 3. | BHB. “Why Some Behavioral Health M&A Is Flying Under the Radar in 2025.” July 2025. |

| 4. | BHB. “Autism Services Deals Hit 5-Year High.” July 3, 2025. |

| 5. | Braff Group. Behavioral health deal tracking data. 2020–2025. |

| 6. | BHB. “7 Autism Therapy Companies to Watch in 2025.” July 2025. |