The Development

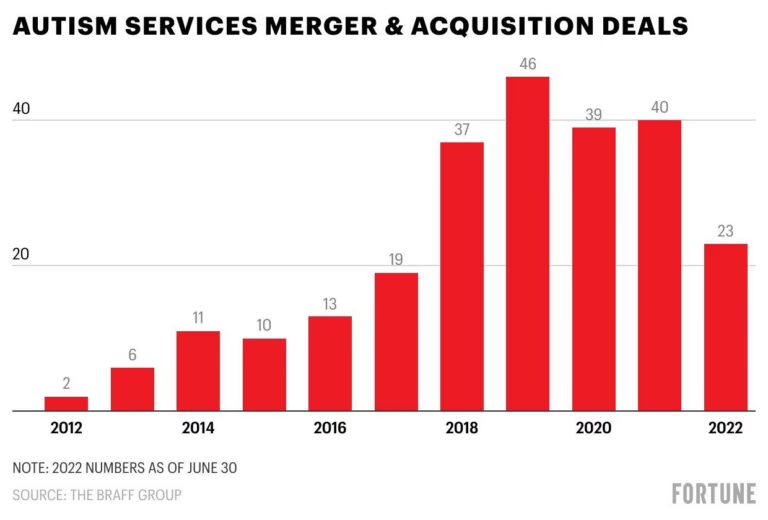

Private equity (PE) firms have dramatically increased their footprint in the autism therapy sector, acquiring 574 centers across 42 states since 2015. The bulk of this activity, nearly 80% of these investments, occurred between 2018 and 2022, marking a rapid expansion phase. This trend is detailed in new research published in JAMA Pediatrics, which sheds light on the drivers behind this significant capital influx into behavioral health.

The study utilized data from PitchBook, identifying PE acquisitions between January 1, 2015, and December 31, 2024, using keywords such as “autism,” “autism treatment facilities,” and “ABA services.” This data was then meticulously verified through public records, press releases, and company documentation to ensure accuracy. The findings indicate a clear correlation between PE entry and specific market conditions, particularly the prevalence of autism spectrum disorder (ASD) diagnoses and the regulatory landscape concerning insurance mandates.

Market Impact

The surge in private equity investment is closely linked to the escalating demand for autism services, fueled by a significant rise in ASD diagnoses. The Centers for Disease Control and Prevention (CDC) data shows a notable increase in prevalence, from 1 in 68 children in 2014 to 1 in 31 in its most recent reporting. This growing patient population presents a compelling market opportunity for investors seeking growth in the healthcare sector.

Geographically, the study found that states with higher autism prevalence and more robust insurance mandates experienced greater private equity involvement. Specifically, states ranking in the top percentile for ASD diagnoses prevalence saw a 24% increase in the likelihood of PE entry. California, Texas, Colorado, Illinois, and Florida emerged as the states with the highest rates of private equity acquisitions during the analyzed period, reflecting concentrated investment in high-demand regions. Conversely, 16 states reported either one or zero private equity-owned autism services, indicating uneven market penetration.

While private equity has long been active in various healthcare segments, including mental health, its specific role and impact on autism services have remained less clear until this research. The study authors noted, “The rapid increase in PE investments in the ASD therapy market coincided with the large increase in childhood ASD diagnoses.” However, they also highlighted an important caveat: “PE entry was associated with ASD prevalence, but it is unclear whether entry led to increased availability of and accessibility to ABA services.” This raises questions about whether investment translates directly into improved patient access or merely consolidates existing services.

Historically, private equity involvement in healthcare has drawn scrutiny due to potential conflicts between investor incentives and patient care goals. Critics often point to instances of staff reductions, pressure on compensation, and a focus on volume growth and expansion, which may not always align with the industry’s broader shift towards value-based care models. Payers, increasingly demanding evidence of outcomes and adherence to quality standards, may find these investment-driven strategies at odds with their expectations for accountability and cost-effectiveness in total care. The authors of the JAMA Pediatrics study underscored these concerns, stating, “Given concerns about PE involvement in ASD services and other health care sectors, further study is needed to determine potential implications for children with ASD.”

What’s Next

As the autism services market evolves, providers anticipate a shift away from “cookie-cutter approaches and old models” in 2026. The landscape for both providers and private equity investors is expected to be shaped by ongoing market uncertainties and increasing demands from payers for demonstrable outcomes and strict adherence to clinical standards. This pressure for evidence-based practice and accountability could influence future investment strategies, potentially pushing PE firms to prioritize value and quality metrics alongside traditional growth objectives.

The findings suggest that while private equity has identified a lucrative market in autism services, the long-term implications for service quality, accessibility, and the professional landscape for behavior analysts remain subjects for continued observation and research. The industry will likely see further consolidation, but with an added emphasis on proving the efficacy and cost-effectiveness of ABA interventions to satisfy both regulatory bodies and a more discerning payer environment.

Fast Facts

| Key Point | Why It Matters for ABA |

|---|---|

| 574 autism centers acquired by PE since 2015 | Highlights rapid consolidation and market shift |

| 80% of investments 2018-2022 | Indicates recent acceleration of PE activity |

| ASD diagnoses increased from 1 in 68 to 1 in 31 | Drives demand for ABA services and investor interest |

| Top prevalence states saw 24% higher PE entry | Shows targeted investment in high-need regions |

| Concerns about PE incentives vs. patient care | Prompts scrutiny on service quality and accessibility |

Expert Perspective

The rapid influx of private equity into autism services underscores a critical need to balance market growth with unwavering commitment to quality and accessibility for children with ASD.

Source: bhbusiness.com