The Growth-to-Proof Transition

ACROSS THE UNITED STATES — An emphasis on measurement-based care, accountability, and defending value are the trends that will transcend across the autism care sector in 2026 amid intensified scrutiny and market pressures. Payer demands and the federal government’s crackdown on waste, fraud, and abuse are driving providers to focus on proving value via measurements and data, as well as on cost containment, according to industry insiders surveyed by Behavioral Health Business. The transition from growth to proof is not a prediction—it is already underway.

Leonard Jeger, CEO of BrightBridge ABA, told BHB that providers will be expected to present robust, transparent performance metrics that objectively demonstrate their effectiveness and value in order to maintain their position within the market. The statement reflects a fundamental shift: for the past decade, the primary challenge for ABA providers was scaling capacity to meet demand. In 2026, the primary challenge is justifying the capacity that has already been built.

Jeff Beck, co-founder and CEO of AnswersNow, was more blunt at the Autism Investor Summit. He stated that as an industry, ABA has dug itself into a hole, and that payers have no empathy for providers who have been billing 40 hours per week and $75,000 per year for the same child for five years without any quality scores. Beck proposed that more providers take on risk-based arrangements that tie revenue to outcomes, arguing that the current fee-for-service model incentivizes volume over value.

Dr. Daniel Spiegel, senior vice president of growth and development at Soar Autism Center, predicted that the biggest factor shaping the market in 2026 will be heightened cost scrutiny from payers, which will push providers toward more efficient, integrated care models. Rather than relying on legacy 40-hour-per-week ABA-only models, the market will shift toward holistic, multidisciplinary approaches delivered at clinically appropriate, cost-effective dosages.

As an industry, we’ve dug ourselves into this hole. And the payers themselves have no empathy for the ABA providers who have been billing them 40 hours a week and $75,000 a year for the same kid for five years without any quality scores.

The Payer Pressure Intensifies

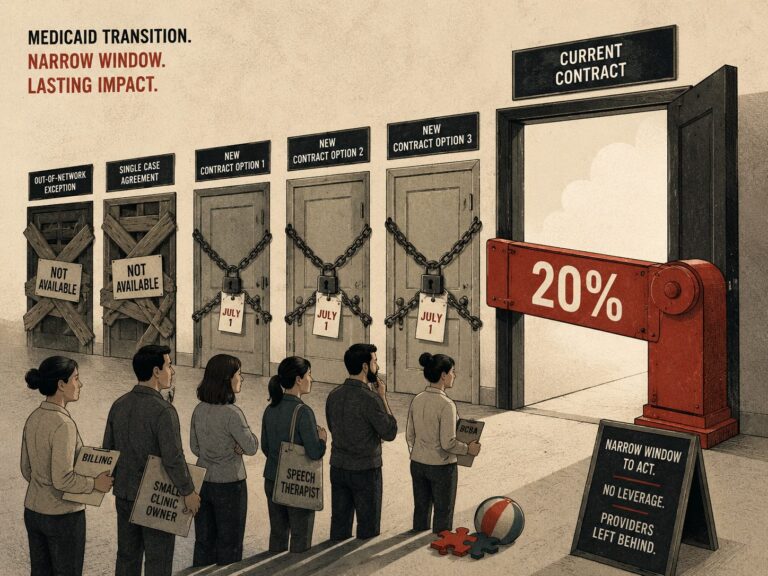

The autism therapy industry is likely in for a rough 2026 as payers of all types seek to control spending. Industry insiders report that rate reductions have already occurred and will likely result in a sustained downward trajectory for both reimbursement rates and approved clinical hours. On top of that, it will be the norm to see what one executive described as a crushing number of audits, a tougher prior authorization process, and other increasingly aggressive behaviors by payers.

The state-level actions are already documented. Nebraska implemented a 48 percent rate cut to ABA services. Indiana instituted cuts in 2023 and later proposed lifetime caps on ABA service hours. Colorado and North Carolina have both proposed cuts to autism funding, with providers and patients suing to challenge the changes. Autism Learning Partners, a major provider in Texas, exited the state entirely, citing low Medicaid rates and administrative burdens. These are not isolated incidents—they represent a pattern of payer behavior that is reshaping the industry’s economics.

At the national level, Centene announced in late 2025 that it was forming a task force to address spending for ABA services, collaborating with state partners on precision in ABA clinical service definition and more stringent supervisory and caregiver engagement requirements. Commercial insurers are approving hours more carefully and requiring stronger documentation for continued care. Underutilized authorized hours remain a concern, with many organizations unable to deliver all approved time due to staffing challenges or scheduling inefficiencies.

The federal dimension adds another layer of pressure. The One Big Beautiful Bill Act, signed into law in July 2025, cuts approximately $1 trillion from Medicaid over 10 years—cuts that will begin taking effect in late 2026. With federal Medicaid cuts on the table, the downward pressure on ABA reimbursement rates is unlikely to ease. The Braff Group’s Dexter Braff noted that while OBBBA provisions largely take effect in 2027, the uncertainty alone is already affecting M&A activity and investor confidence in the sector.

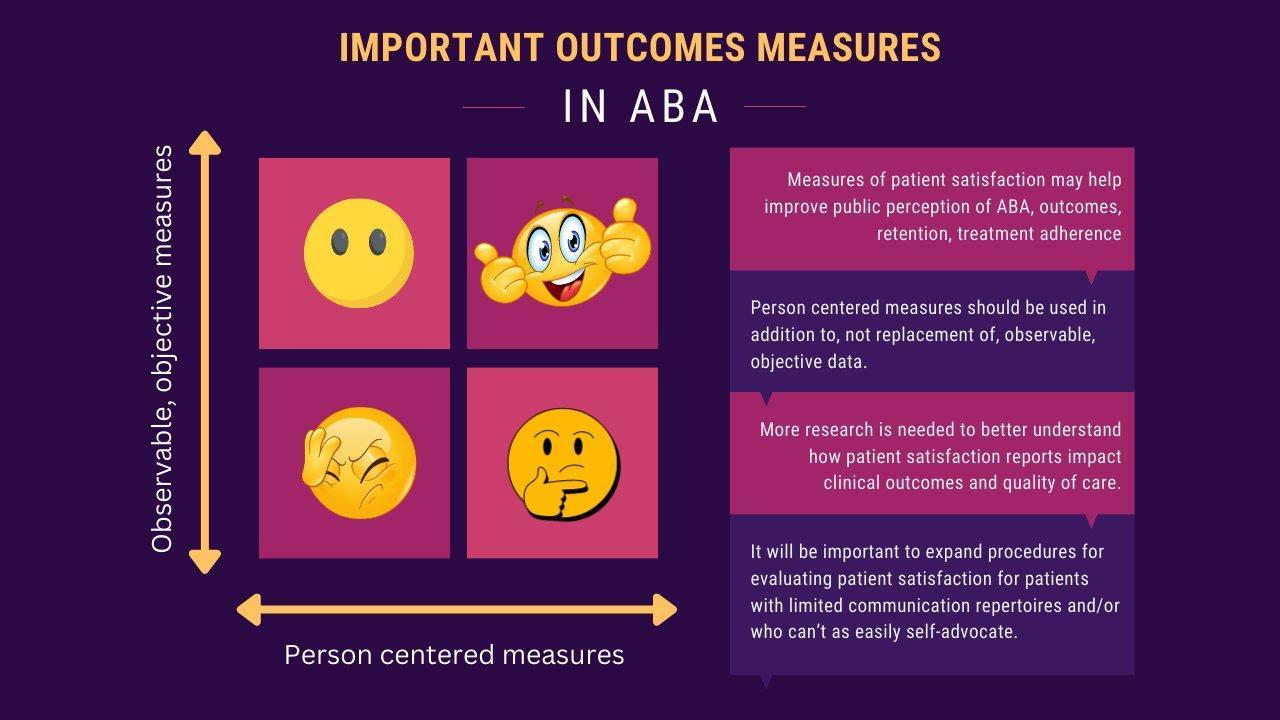

The Outcomes Measurement Imperative

Jim Spink, CEO of Autism Care Partners, framed the challenge at the Autism Investor Summit East: it is necessary to have standardized data sets moving forward to be a value-based provider beyond just some of the process measures. Until the industry gets there, real value-based contracts will remain few and far between. The warning is clear: if providers do not lead the conversation about standardizing outcomes measures, payers will define those measures for them—and the resulting framework may not reflect clinical reality.

The ABA field is uniquely positioned for outcomes measurement. ABA therapy routinely collects trial-by-trial behavioral data during sessions. Therapists measure skill acquisition, behavior reduction, and engagement continuously, often generating hundreds of data points per session. This granular clinical data creates an opportunity: when aggregated, interpreted, and made visible, these data streams can position autism care organizations to demonstrate value with a level of transparency that other behavioral health sectors are still trying to achieve.

But granular data is not the same as meaningful outcomes. The industry still lacks standardized definitions of what constitutes a good outcome in ABA. Is it mastery of specific skills? Reduction in challenging behaviors? Improvement in adaptive functioning as measured by validated instruments like the Vineland? Parent satisfaction? Quality of life? All of the above? The absence of industry-wide standards means that every provider measures different things in different ways, making comparison impossible and payer evaluation inconsistent.

Value-based care conversations are heating up across behavioral health, though they remain few and far between in the autism space specifically. Some insurance contracts for ABA already include quality incentives or reporting requirements—providers may need to document progress every six months to justify continued services. But these are early experiments, not established models. The transition from fee-for-service to outcomes-based reimbursement in ABA is a multi-year process that requires standardization, technology infrastructure, and willingness from both providers and payers to share risk.

If providers do not lead the conversation about standardizing outcomes measures, payers will define those measures for them. And the payer-defined framework may not reflect clinical reality.

Consolidation as a Survival Strategy

With sustained downward pressure on rates and hours, more companies will be forced to consolidate or exit the market. Mike Cairnes, CEO of JoyBridge Kids, noted that the industry is moving toward a tipping point where consolidation will accelerate and bad players will be forced to exit. The ABA industry remains highly fragmented, and the current pressures are beginning to separate providers who invested in quality from those who scaled on volume alone.

Goldman Sachs’ Jason Slocum, managing director of sustainable investing, said the firm is in the second phase of autism investment, with tremendous unmet need and consolidation opportunity remaining. But he emphasized that as an investor, the firm is thinking very hard about making sure it is on the right side of healthcare and the right side of where payers are trying to go within ABA. The message to providers seeking investment or acquisition: demonstrating payer relationships and outcomes data is now as important as demonstrating revenue growth.

Companies will also need to establish cultures that focus on both quality and efficiency, coupled with technology, to make up the difference from lost rates. Technology alone is not the answer, but there is no doubt it is a key component if the industry has any hope of driving a more efficient system, said Steve Brasch, an industry consultant. Providers who combine outcomes measurement, technology adoption, and operational efficiency will be the ones that attract capital and survive the current downturn.

For practice owners and clinical directors, the message from 2026 is unambiguous: the era of growth for growth’s sake is over. The ABA industry must prove that its services produce measurable, meaningful improvements in the lives of the children and families it serves. Providers that can demonstrate this proof will thrive. Providers that cannot will find themselves on the wrong side of a market that no longer rewards volume alone.

The year 2026 will be remembered as the inflection point where the ABA industry’s relationship with its payers fundamentally changed. Whether that change produces a healthier, more sustainable industry or a contraction that reduces access to care depends entirely on whether providers embrace the transition to proof—or resist it until the choice is made for them.

AT A GLANCE

| Industry transition: | Growth mode to proof mode (BHB, Dec 2025) |

| Payer actions: | Nebraska 48% rate cut; Indiana lifetime hour caps; CO and NC proposed cuts |

| Centene: | ABA spending task force formed late 2025; precision in clinical service definition |

| OBBBA Medicaid cuts: | ~$1 trillion over 10 years; provisions take effect late 2026–2027 |

| ALP Texas exit: | Autism Learning Partners exited Texas citing low Medicaid rates |

| Industry quote (Beck): | Payers have no empathy for 40hr/wk, $75K/yr billing without quality scores |

| VBC status: | Few value-based ABA contracts exist; conversations accelerating |

| Key metric gap: | No standardized industry-wide ABA outcomes measures |

| Goldman Sachs view: | Second phase of autism investment; outcomes data now critical in due diligence |

| Technology role: | Essential for outcomes aggregation, billing efficiency, and clinician productivity |

SOURCES & REFERENCES

| 1. | BHB. “Behavioral Health in 2026 Will Transition From Growth to Proof.” December 31, 2025. |

| 2. | BHB. “We’ve Dug Ourselves Into This Hole: What It Takes for Autism Providers to Succeed.” March 2, 2026. |

| 3. | BHB. “Autism Care Faces Market Reckoning as Payers, Investors Push for Proof of Outcomes.” November 2025. |

| 4. | BHB. “Behavioral Health Predictions for 2026: Autism Rate Cuts, TMS on the Rise.” January 2026. |

| 5. | ABA Matrix. “ABA Trends 2026.” December 2025. abamatrix.com. |

| 6. | Hi Rasmus. “What the 2026 VALUE Conference Revealed About Value-Based Care.” March 2026. |