An Opinion Editorial

A company-wide email notifies the staff on Monday morning. A new ownership group has finalized its acquisition. By Friday, several clinical directors have been eliminated, a new CFO brought in, productivity levels raised, and expenses have been slashed.

Nobody asked the BCBAs. Nobody asked the families. Nobody asked the kids. I will never forget when a private equity partner, who had owned an ABA company for two years, asked me “what do BCBA stand for?”

This is not a hypothetical. This is the lived reality of what happens when what I call “traditional private equity” enters the field of Applied Behavior Analysis — and it is happening with alarming frequency.

As someone who has worked in and around ABA services, I want to say plainly what too many in our industry whisper but rarely commit to print: not all investors are the same, and the difference between a “traditional private equity firm” and a “clinically-minded capital partner” is radically different. It is the difference between a practice that flourishes and one that bills CPT codes for profit.

The Traditional PE Playbook: Managing by Spreadsheet

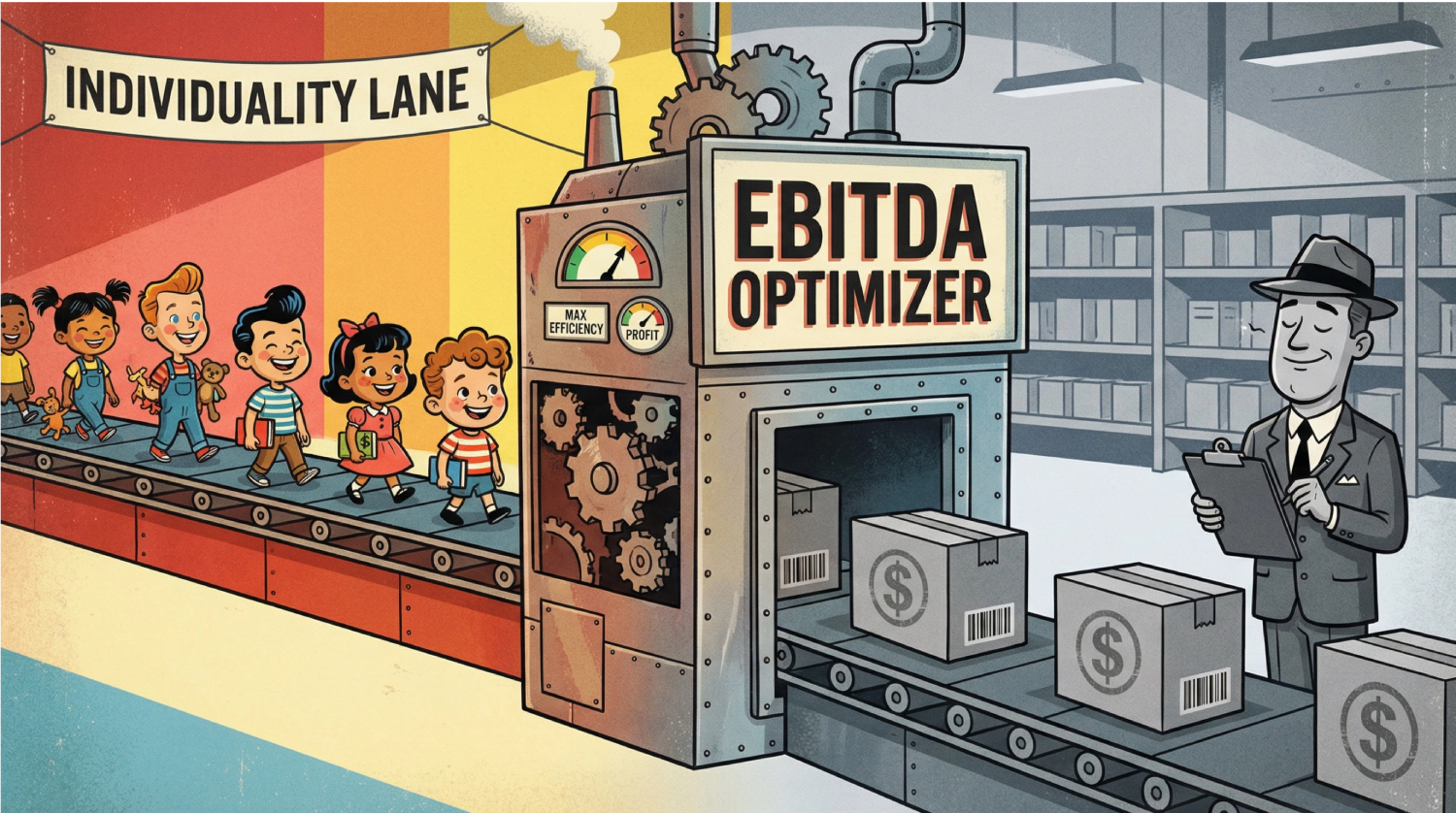

Private equity has a formula, and it works beautifully for widget factories. Buy a business, cut costs aggressively, optimize for EBITDA (Earnings Before Interest Taxes Depreciation and Amortization), and sell within five years for a multiple. Rinse. Repeat.

The problem is that ABA is not a widget factory. The “product” is a child with autism learning to communicate, to connect, to navigate the world. You cannot optimize that on a spreadsheet without causing harm — but traditional PE tries anyway.

Here Is What It Looks Like In Practice:

They slash headcount first and ask questions later. Clinical supervisors are expensive. Regional directors are expensive. Senior BCBAs and training professionals are expensive. So they go. What remains is a skeleton crew of staff stretched impossibly thin, supervising far more clients than is clinically appropriate, cutting corners not because they want to but because they are in survival mode.

They commoditize therapists. Behavior Technicians — the frontline workers who spend hours each day building relationships with children — are treated as interchangeable, low-cost labor.

Slash wages. Cut benefits. Turnover explodes. And every time a child’s RBT quits, that child regresses. Relationships built over months are severed. Families start the painful process of rebuilding trust with yet another stranger. Traditional PE does think of this as a cost. But it is very real.

They centralize clinical decisions. Suddenly, the number of hours a child receives is not determined by their individualized treatment plan or a BCBA’s professional judgment. It is determined by revenue targets, what keeps the schedule full, and what fits their “business model”. The ethics code that BCBAs are bound to professionally begins to feel like an obstacle rather than a foundation. Stories abound of management changing a BCBA’s recommended treatment hours, or establishing minimum hours for each client.

They manage toward an exit (when they flip the company to another buyer), not toward outcomes. The five-year holding period is not a secret. Every decision made under traditional PE ownership is made with one eye on the eventual sale. Long-term infrastructure investments that would improve clinical quality — robust training programs, clinical mentorship pipelines, technology systems that actually support care coordination — are deferred or eliminated. Why invest in something you plan to sell?

They replace mission with metrics. Utilization rates. Authorization conversion. Revenue per billable hour. These become the language of the organization. “Are kids making progress?” becomes a question that is no longer asked.

A quick Google search will reveal several incredible ABA companies that traditional private equity destroyed in a few short years. It does not have to be this way.

The Clinically-Minded Capital Partner: A Fundamentally Different Animal

Now let me describe a different experience — one that is possible, that exists, and that the field desperately needs more of.

A clinically-minded capital partner enters an ABA organization and does something radical: it listens. It sits with the clinical leadership. It asks what resources are missing. It asks what is getting in the way of delivering great care. And then — here is the revolutionary part — it actually tries to fix those things.

They invest in the clinical model, they do not gut it. Where traditional PE sees a clinical director as a cost center, a clinically-minded partner sees them as the foundation of the entire enterprise. They fund clinical infrastructure. They build or improve training programs. They hire senior BCBAs rather than eliminating them. They understand that clinical excellence is not separate from business sustainability — it IS the business.

They protect clinician autonomy fiercely. A good capital partner knows the boundary between business operations and clinical practice, and they do not cross it. Treatment decisions belong to the clinician. Hours are determined by what a child needs. The BCBA’s professional judgment is not overruled by a revenue cycle manager they have never met. This is not just ethically correct — it is legally correct. And partners who understand the field know it.

They invest in people as if they plan to stay. Competitive wages. Career ladders. Clinical mentorship. A culture where RBTs feel valued and BCBAs feel supported. The result is retention — and retention in ABA is everything. A child who keeps the same therapist for two years makes progress that a child cycling through twelve therapists in two years simply cannot replicate. Clinically-minded investors understand this. They fund it accordingly.

They think long term. Rather than engineering a five-year exit, a genuine clinical partner thinks about what this organization needs to look like to still be serving families well. They make long-term capital investments. They build for scale that doesn’t sacrifice quality. They understand that the reputational and human cost of poor outcomes far exceeds any short-term margin gain.

They measure what actually matters. Yes, they watch the financials — they must. But they also track clinical outcomes. They ask whether kids are making progress. They look at family satisfaction. They monitor BCBA burnout rates and take them seriously. The metrics of a clinically-minded partner reflect a belief that good outcomes and good business are not in tension — they are the same thing.

This Distinction Has Never Mattered More

ABA is in a moment of enormous growth. Autism diagnoses continue to rise. Insurance mandates have expanded access dramatically. The demand for services has never been higher — and capital is following that demand.

Private equity money is gushing into ABA. Some of it will be the right kind. Much of it is not.

Families choosing providers deserve to understand this. BCBAs considering employment at organizations deserve to ask hard questions: Who owns this? What is their track record? Do clinical leaders have a seat at the table or a seat in the waiting room?

And for those of us who love this field — who got into it because we believe in its power to change lives — we have an obligation to say clearly: the source and character of capital in ABA therapy is a clinical issue, not just a business one. Who owns a practice shapes what that practice does for children. It determines whether an RBT shows up tomorrow or burns out and quits. It shapes whether a BCBA can practice with integrity or has to choose between ethics and employment.

The children we serve did not choose their investors. We owe it to them to choose carefully on their behalf.