Scale That No Other State Can Match

TALLAHASSEE, FLORIDA – the number that stops a room full of ABA operators is not from California or Texas. It is from Florida. In December 2024, state economists told Florida’s Agency for Health Care Administration that for fiscal year 2024–25, the state’s Medicaid program was on track to spend approximately $2.62 billion on behavior analysis services. That figure—reported by the Florida Phoenix—encompasses both the legacy fee-for-service system that governed ABA spending through January 2025 and the new Statewide Medicaid Managed Care contracts that took effect in February 2025 and transferred most ABA spending into managed care plans. By any measure, it is the largest single-state Medicaid ABA expenditure in the country.

The scale reflects both genuine demand and a structural environment that, over more than a decade, made Florida one of the most attractive states in the country for ABA providers of every size and type. Florida enacted Senate Bill 2654—the state’s autism insurance mandate—in 2008, among the earliest such mandates in the country. The law required large group health plans and HMOs to cover ABA therapy beginning April 1, 2009. It capped annual commercial insurance benefits at $36,000 per year and set a lifetime limit of $200,000—restrictions that remain lower than many competing states and that, in practice, have pushed intensive therapy costs onto Medicaid for the lowest-income families.

The state’s autism population justifies the scale. According to CDC and market data, Florida is home to an estimated 329,131 adults with autism spectrum disorder—the fourth-highest figure of any state in the nation, behind California, Texas, and New York. The childhood diagnosis rate mirrors national trends: 1 in 31 children as of the CDC’s 2025 ADDM Network data. Florida Medicaid serves more than 4.3 million beneficiaries, and the program covers BA services for all Medicaid-eligible recipients under age 21 for whom the treatment is medically necessary under the federal EPSDT mandate. For those 21 and older, coverage continues through the iBudget Waiver, Florida’s Home and Community-Based Services program for individuals with developmental disabilities.

For ABA providers and the private equity firms that have backed them, Florida’s combination of large population, early insurance mandate, open Medicaid coverage, and year-round climate for clinical operations created a growth corridor with few rivals. According to a January 2026 study published in JAMA Pediatrics by researchers at Brown University, Florida ranked among the top five states by total private equity acquisition of autism therapy centers, alongside California, Texas, Colorado, and Illinois. The study found that states in the top tier of childhood autism prevalence were 24 percent more likely to have PE-owned clinics. Florida sits firmly in that tier.

Florida’s Medicaid program was projected to spend approximately $2.62 billion on behavior analysis therapy in fiscal year 2024–25 — the largest single-state Medicaid ABA expenditure in the country. — Florida Phoenix, citing state economist testimony, December 2024

What Made Florida the Preferred Market

The ABA market does not distribute itself randomly across states. It concentrates in places where payer coverage is broad, reimbursement rates are workable, the population density supports clinic economics, and the regulatory environment does not create excessive barriers to entry or credentialing. Florida has consistently scored well on each of these dimensions in ways that neighboring states have not.

Early mandate with open Medicaid coverage: Florida’s 2008 commercial insurance mandate was among the first in the Southeast, placing it ahead of most competing states in establishing a commercial payer base for ABA. More significantly, Florida’s Medicaid program covers BA services under the EPSDT benefit without the stringent hour caps or lifetime service limits that some state Medicaid programs have imposed. Until February 2025, Florida Medicaid covered BA services under a fee-for-service system, allowing providers to bill directly for authorized hours at state-set rates. The combination of commercial mandate plus open-ended Medicaid coverage gave Florida providers two distinct reimbursement channels, each serving a different income strata of the same patient population.

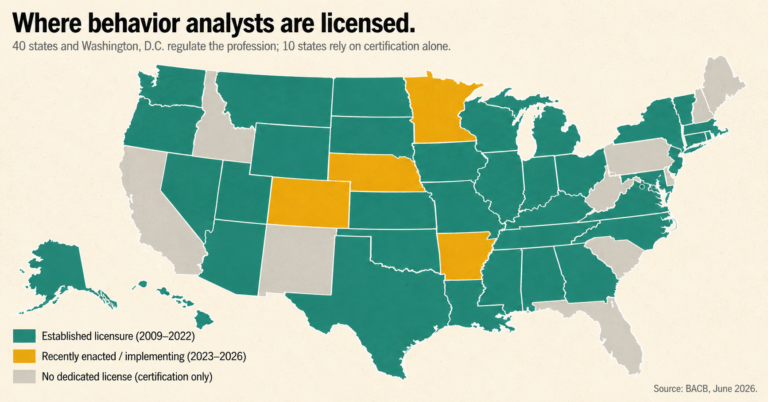

No state BCBA licensure law: As of 2025, Florida remains one of approximately ten states that have not enacted a formal state licensure law for behavior analysts. While Florida’s Medicaid program requires that lead analysts hold BCBA certification from the Behavior Analyst Certification Board, and while non-Medicaid providers must be licensed under the Florida Health Care Clinic Act, the absence of a standalone state licensure framework created a lower barrier to market entry than the 40 jurisdictions that now require formal state licensure. The Florida Association for Behavior Analysis has been a consistent voice on this issue, but no BCBA licensure legislation has cleared the Florida Legislature as of the date of publication.

Workforce economics: Florida’s warm climate and growing metropolitan areas have made it a destination for behavior analysts relocating from colder markets. The Bureau of Labor Statistics projects 29 percent employment growth for the category that includes behavior analysts and counselors in Florida between 2022 and 2032—nearly double the national projection of 17 percent. As of May 2024, Florida employed 24,680 professionals in this occupational category, with a statewide median salary of $56,830. The state’s large university system produces a continuous pipeline of BCBA candidates.

Geographic diversity: Unlike Nebraska, whose population is concentrated in two metro areas, Florida offers multiple distinct metropolitan corridors—Miami–Fort Lauderdale, Tampa–St. Petersburg, Orlando, Jacksonville, and a string of smaller coastal markets—each capable of supporting multi-site center-based operations at scale. The Southeast U.S. region, of which Florida is the largest single-state component, accounted for 31.8 percent of total U.S. autism clinic market revenue in 2023, the largest regional share in the country, according to market research firm NovaOne Advisor.

The Fraud Vector: Miami-Dade and What It Reveals

The same conditions that made Florida attractive to legitimate ABA providers—broad coverage, accessible credentials, high reimbursement—also made it attractive to fraudulent ones. The evidence of that dynamic is most concentrated in Miami-Dade County, which by Florida’s own data has functioned as the state’s dominant ABA revenue center and its primary fraud enforcement zone simultaneously.

According to NBC6 Investigates, citing Florida Medicaid data for 2023–2024, of the approximately $1.5 billion paid for ABA services in Florida during that period, more than half was billed from Miami-Dade County. The concentration is not explained by population alone: Miami-Dade accounts for roughly 14 percent of Florida’s total population. That billing share is a function of both the county’s large Medicaid-eligible autism population and a years-long pattern in which the county has attracted disproportionate numbers of high-volume ABA billing operations, some of which have been the subjects of federal investigation.

In May 2018, AHCA determined that some providers of ABA services in Miami-Dade and Broward counties had falsified enrollment credentials and engaged in fraudulent billing practices, and obtained approval from the Centers for Medicare and Medicaid Services for a moratorium on new ABA provider enrollment in those two counties. The moratorium, initially authorized for six months, was extended repeatedly in six-month increments and remained in effect in various forms through at least 2022—a four-year span during which Florida’s AHCA restricted new provider entry into the market it had identified as highest risk.

The moratorium did not end the fraud. Florida’s MFCU annual report for fiscal year 2023–24 disclosed that the agency’s Miami field office conducted 162 site visits to behavioral health service providers not linked to a specific physician enrolled with Medicaid. Of those 162 providers, 117—or 72 percent—were not operational at their service address of record. They had collected Medicaid billing authorizations but did not maintain a functioning clinical presence at the locations they had listed with the agency.

The credential fraud problem manifested at a different level of the workforce. HHS Office of Inspector General investigators in Miami documented a specific pattern of RBT examination cheating in South Florida, sharing video footage with NBC6 Investigates showing a woman, Grisel Farinas, receiving coaching during a remotely administered RBT certification exam. According to Fernando Porras, Assistant Special Agent in Charge with HHS/OIG in Miami, Farinas paid approximately $2,000 to have someone guide her through the exam in real time. The certification exam companies, recognizing the scope of the problem, ended remote proctoring for RBT tests in March 2021.

Of 162 site visits to behavioral health providers in Miami-Dade not linked to a specific physician, 117 — 72 percent — were not operational at their service address of record. — Florida AHCA, Annual Report on Medicaid Fraud and Abuse, FY 2023–24

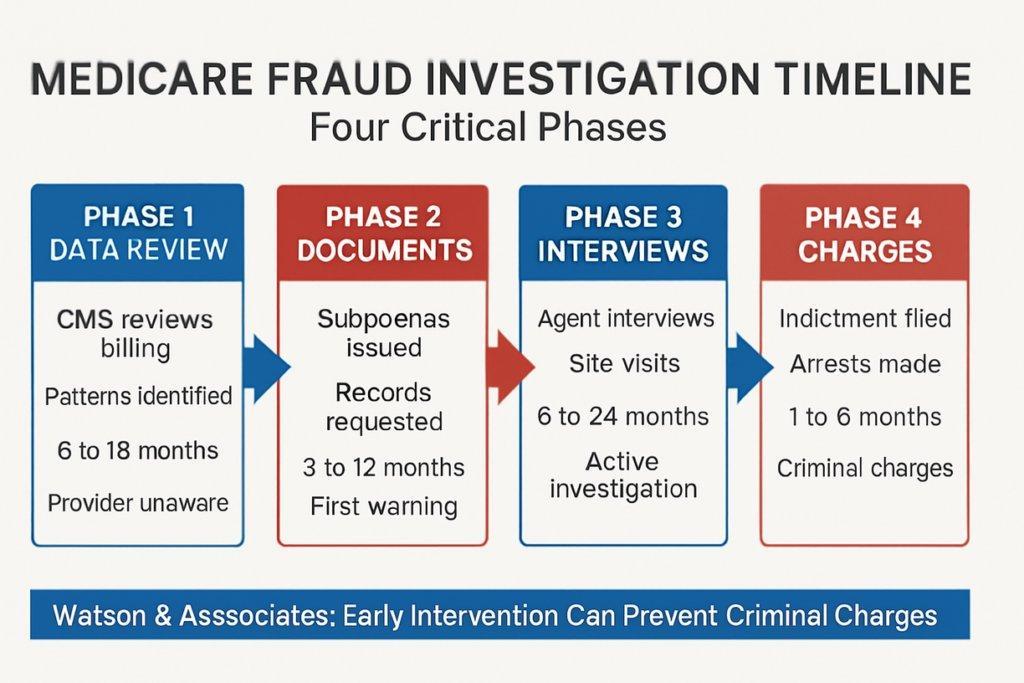

The cost-doubling that WUSF documented between 2016 and 2018, driven in part by unqualified providers billing for unnecessary services, precipitated the moratorium but also illustrated the speed at which a regulatory gap can be exploited in a state without a licensure floor. Florida’s responses—the moratorium, the rollout of Electronic Visit Verification as a pilot in South Florida starting September 2019, and the enhanced credentialing requirements AHCA imposed in 2018 and 2019—addressed symptoms without closing the underlying structural vulnerability. As the federal investigation timeline diagram above illustrates, billing data anomalies typically precede enforcement action by 6 to 18 months: a provider flagged in Phase 1 may continue billing for the duration of a full document review and interview cycle before any charges materialize.

The 2025 Structural Shift: ABA Moves Into Managed Care

Beginning February 2025, Florida executed the most significant structural change to its ABA Medicaid program since the initial coverage mandate. Under new SMMC contracts effective through 2030, BA services were transferred from the state’s legacy fee-for-service system into the Statewide Medicaid Managed Care program, which operates through nine regional managed care plans. Providers who had billed Medicaid directly for authorized hours now must be in-network with the managed care organization—Aetna Better Health, Sunshine Health, Florida Community Care, Simply Health, Humana, Molina, or UnitedHealthcare—covering the child’s enrollment region.

The transition carries significant implications for market structure. Under fee-for-service, any credentialed provider authorized by AHCA could bill for Medicaid clients regardless of plan affiliation. Under SMMC, access depends on network contracting. Smaller providers operating in single counties may find that MCO contracting requirements, credentialing timelines, and network rate negotiations create meaningful barriers that did not exist under fee-for-service. Larger multi-site operators with established MCO relationships and billing infrastructure are comparatively advantaged. The shift is a de facto consolidation mechanism: it will reduce the number of providers serving Medicaid clients by attrition among those who cannot or will not negotiate network contracts.

The fraud-control implications are also material. Managed care organizations are contractually required by AHCA to maintain anti-fraud units, submit Annual Fraud and Abuse Activity Reports, and conduct internal investigations of potential fraud and overpayment. Managed care introduces a layer of prior authorization review and claims adjudication between the provider and the state that fee-for-service lacked. In theory, this reduces the ability of a fraudulent provider to bill freely once enrolled. In practice, AHCA’s own oversight audit published in January 2024 noted significant variation in plan-level anti-fraud activities across fiscal years 2020–22, and the MCO anti-fraud performance on ABA specifically remains an open question as the new contracts mature.

For the industry’s legitimate operators, the transition created a period of operational uncertainty. The Florida Association for Behavior Analysis reported member concerns about authorization transitions, billing system changes, and the mechanics of continuity-of-care protections as children moved from fee-for-service to managed care. The February 2025 transition deadline, which required providers to be contracted with specific MCO networks to continue serving Medicaid clients, produced access disruption that the agency acknowledged required active monitoring.

The Market Map: What Florida Means for Industry Strategy

For ABA operators and investors reading Florida as a state market, the picture that emerges is neither uniformly positive nor uniformly cautionary. Florida is simultaneously the clearest demonstration of what a large, early-adopting insurance mandate state can become and the clearest demonstration of what happens when that market grows faster than its oversight infrastructure.

The private equity playbook for Florida has followed the national pattern with local concentration. The JAMA Pediatrics study identified Florida among the top five states for PE-backed autism center acquisitions, with the Southeast broadly representing nearly a third of the national market by revenue. Large national operators—including chains that have expanded from Texas and Indiana—have entered the Florida market at multiple points over the past decade, drawn by the combination of commercial and Medicaid payer mix, workforce availability, and the absence of licensure barriers.

The structural risks are not academic. The moratorium experience documented that the Florida market can be destabilized by fraud at sufficient scale to require a multi-year enrollment freeze in its two highest-revenue counties. The RBT credentialing fraud documented by HHS/OIG illustrates that a workforce entry point without a state licensure floor creates an attack surface that sophisticated fraud networks have been willing to exploit. The 72 percent ghost provider rate documented in AHCA’s own site visits to Miami behavioral health providers is the kind of figure that, in any other sector of healthcare, would have triggered a federal audit of the magnitude seen in Indiana, Wisconsin, and Colorado. No such OIG audit of Florida’s ABA program has been published to date.

The SMMC transition adds a new dimension of uncertainty that will take multiple years to resolve. Whether managed care reduces fraudulent billing, expands or contracts access for legitimate providers, and whether the MCOs can responsibly manage a $2-plus billion annual ABA benefit are questions that Florida’s health care infrastructure will spend the next contract cycle—through 2030—answering. The state’s response to that test will determine whether Florida’s ABA market matures into a well-governed system that can sustain the investment it has attracted, or whether it follows the arc of states where rapid growth preceded accountability—and accountability proved expensive.

AT A GLANCE

FL Medicaid ABA projected spend (FY 2024–25): ~$2.62 billion (fee-for-service July 2024–Jan 2025: ~$1.63B; SMMC Feb–June 2025: ~$1B) — Florida Phoenix / state economist testimony, Dec. 2024

FL autism insurance mandate enacted: Senate Bill 2654, 2008; effective April 1, 2009 — among the nation’s earliest state mandates

Commercial mandate caps: $36,000/year; lifetime limit $200,000 (large group fully insured plans and HMOs)

BCBA state licensure in Florida: No standalone BCBA licensure law as of 2025; BACB certification required for Medicaid enrollment only

FL estimated adults with ASD: 329,131 — 4th highest nationally (CDC / GM Insights, 2023)

FL ABA Medicaid SMMC transition: February 2025 — BA services moved from fee-for-service into Statewide Medicaid Managed Care (9 regional plans through 2030)

Miami-Dade ABA billing share (2023–24): More than 50% of Florida’s ~$1.5 billion in ABA Medicaid payments — NBC6 Investigates, July 2024

Ghost provider rate (AHCA site visits): 117 of 162 behavioral health providers (72%) not operational at service address — AHCA FY2023–24 Annual Report

South Florida moratorium: Effective May 14, 2018; Miami-Dade and Broward counties; extended every 6 months through at least 2022

RBT exam cheating: HHS/OIG documented South Florida cases; remote RBT exam proctoring ended March 2021 due to cheating volume

PE market ranking: Florida in top 5 states for PE autism center acquisitions (JAMA Pediatrics, Brown University, January 2026)

EVV for ABA in FL: Piloted September 2019 in Regions 9–11 (South Florida) in response to fraud; among the first states nationally to deploy

SOURCES & REFERENCES

1. – Florida Phoenix. “Lower Medicaid caseloads help offset increasing health care costs.” Christine Sexton. December 23, 2024. floridaphoenix.com. (Citing state economist testimony on $2.62B ABA spending projection, FY 2024–25.)

2. – NBC6 Investigates (South Florida). “Fraud Targeting Resources Meant for Children with Autism.” July 21, 2024. nbcmiami.com. (Miami-Dade billing concentration; RBT exam cheating; HHS/OIG Agent Fernando Porras on record; Grisel Farinas case.)

3. – Florida Agency for Health Care Administration. “The State’s Efforts to Control Medicaid Fraud and Abuse FY 2023–24.” January 2025. ahca.myflorida.com. (162 site visits; 117 of 162 not operational; MFCU enforcement activity.)

4. – Autism Legal Resource Center / Florida CFO Division of Consumer Services. Florida Senate Bill 2654. Enacted 2008, effective April 1, 2009. autismlegalresourcecenter.com; myfloridacfo.com.

5. – Florida Health Justice Project. “Important Change to Behavior Analysis (BA) Therapies for Medicaid Enrolled Children.” August 2025. floridahealthjustice.org. (SMMC transition; managed care plan list; EPSDT appeal rights.)

6. – Florida AHCA. Statewide Medicaid Managed Care (SMMC) New Program Highlight — Behavior Analysis. October 2024. ahca.myflorida.com.

7. – Florida AHCA. Behavior Analysis Services Information. ahca.myflorida.com. (Prior authorization, EVV, credentialing requirements, iBudget Waiver for adults 21+.)

8. – Florida Senate Bill Analysis: HB 1401 (2021). flsenate.gov. (Moratorium history; no BCBA licensure; AHCA credentialing requirements; EVV rollout timeline.)

9. – InBloom Autism Services. “Understanding the South Florida Medicaid Moratorium.” Updated June 2025. inbloomautism.com. (May 2018 moratorium; November 2018 extension; provider access impact.)

10. – Wolfe Pincavage. “Applied Behavior Analysis Therapy Medicaid Enrollment and Licensure in the Sunshine State.” wolfepincavage.com. (Moratorium legal framework; CMS approval; M&A impact.)

11. – WUSF Public Media. “AHCA To Roll Out ABA Therapy GPS Tracking, Other Medicaid Changes.” May 14, 2019. wusfnews.wusf.usf.edu. (Cost doubling 2016–2018; no FL licensure; FABA response; EVV pilot launch.)

12. – Arnold D et al. (Brown University). “Private Equity and Autism Therapy Centers.” JAMA Pediatrics. January 5, 2026. (574 centers across 42 states; Florida in top 5 PE states; 24% autism prevalence correlation.)

13. – Behavioral Health Business. “PE Investment in Autism Services Tracks State Medicaid Rate Increases, Growing Diagnoses.” January 6, 2026. bhbusiness.com.

14. – CEPR. “Pocketing Money Meant for Kids: Private Equity in Autism Services.” September 2025. cepr.net. (PE entry timeline; state mandate relationship; national chain case studies.)

15. – NovaOne Advisor. “U.S. ADHD and Autism Clinics Market.” December 2025. (Southeast region 31.80% U.S. market share in 2023.)

16. – GM Insights / CDC. “U.S. Applied Behavior Analysis Market Size.” 2023–2024. (FL estimated 329,131 adults with ASD; 4th nationally.)

17. – Florida OPPAGA. “Biennial Review of AHCA’s Oversight of SMMC.” Report 24-03. January 2024. oppaga.fl.gov. (MCO anti-fraud requirements; AFAAR reporting; variation in plan anti-fraud activity FY2020–22.)

18. – Applied Behavior Analysis Education. “How to Become a BCBA in Florida.” Updated February 2026. (29% workforce growth 2022–2032; 2,120 annual openings; median salary $56,830; licensure status.)

19. – Trilliant Health. “ABA Therapy Utilization Grew Nearly 300%, Driven by Increases in Medicaid.” December 2025. trillianthealth.com. (267% national growth 2019–2024; Medicaid vs. commercial divergence.)