Business • Mergers & Acquisitions • July 2026

ABA and Pediatric Therapy M&A: What the First Half of 2026 Tells Us About Today’s Buyers

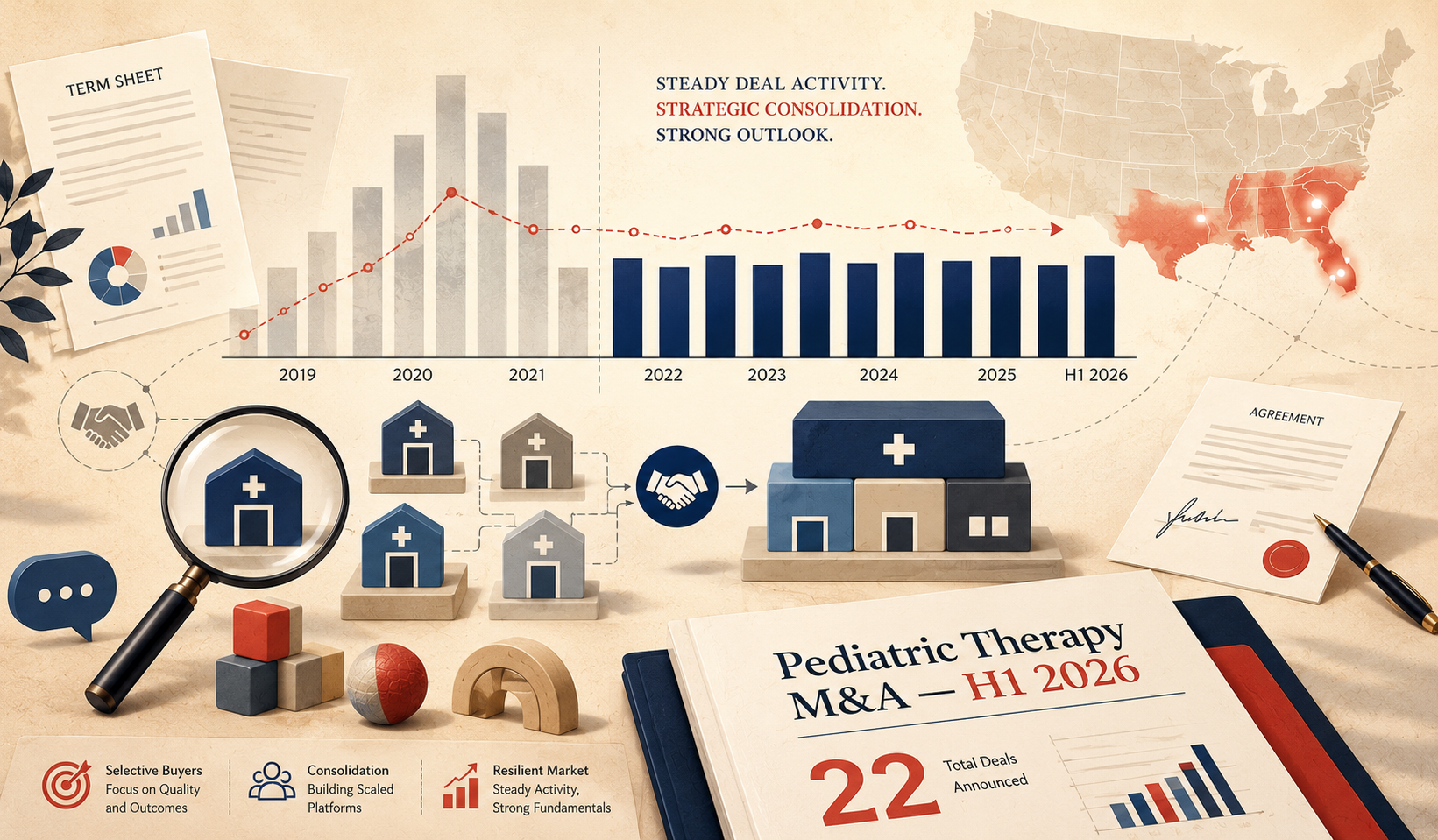

Twenty-two deals in six months signal a market that has stabilized, not stalled — but the buyers writing checks today look nothing like the growth-chasers of 2021. Operational discipline, multidisciplinary care models, and clinic-based scale now separate the practices that command premiums from the ones that don’t.

By Luis Lopez, PhD

After several years of post-pandemic adjustment, the pediatric therapy M&A market appears to have entered a more stable phase. While reimbursement pressures, labor shortages, and operating challenges continue to affect providers across the country, acquisition activity has remained resilient.

Mergium Advisors identified 22 pediatric therapy mergers and acquisitions announced during the first half of 2026, a level of activity that is broadly consistent with the market observed over the past several years, excluding the unusually active transaction environment of 2021 and early 2022.

Although the pace of transactions has normalized, the underlying dynamics of the market continue to evolve. Several themes emerged during the first half of the year that are likely to remain important for founders, operators, and investors.

Private Equity Continues to Drive Industry Consolidation

Private equity-backed platform companies remained the most active acquirers during the first half of 2026, representing nearly two-thirds of announced transactions. This continues a pattern that has characterized the pediatric therapy industry for several years.

Established platform companies continue to expand through add-on acquisitions, while new private equity sponsors also entered the sector by acquiring founder-owned practices to establish new investment platforms. During the first half of 2026, three transactions represented new platform investments rather than follow-on acquisitions.

The continued willingness of financial sponsors to invest in pediatric therapy reflects confidence in the industry’s long-term fundamentals despite current operational headwinds. Demand for autism services, speech therapy, occupational therapy, and related pediatric services continues to benefit from favorable demographic trends and increasing awareness of developmental disorders.

At the same time, investors remain disciplined. Buyers are placing greater emphasis on sustainable margins, operational infrastructure, clinical leadership, and reimbursement quality than they did during the exceptionally competitive market of 2021.

Multidisciplinary Providers Continue to Command Attention

One of the clearest themes during the first half of the year was continued buyer interest in multidisciplinary pediatric therapy organizations.

Many acquisition targets combined Applied Behavior Analysis (ABA) with speech therapy, occupational therapy, physical therapy, counseling, or other pediatric services. These integrated models continue to appeal to both strategic buyers and financial sponsors because they allow providers to serve families across multiple clinical needs while creating opportunities for operational leverage and referral synergies.

This trend does not diminish the attractiveness of pure-play ABA organizations. Rather, it suggests that buyers increasingly value businesses capable of expanding service offerings, diversifying referral relationships, and serving children throughout a broader continuum of care.

Buyers Continue to Favor Scalable Operating Models

The delivery model also remained an important characteristic of acquisition targets.

Clinic-based providers represented the largest share of announced transactions during the first half of the year, while school-based providers also maintained meaningful acquisition activity. Although home-based services remain an important component of the industry, many investors continue to view clinic-centered operations as offering greater scalability, operational consistency, and scheduling efficiency.

That does not mean one delivery model is inherently superior. Successful providers operate across all settings. However, buyers continue to evaluate how each operating model affects staffing, supervision, utilization, scheduling, and long-term profitability.

Employee Ownership Remains Uncommon

One noteworthy transaction involved North Arrow ABA’s adoption of an Employee Stock Ownership Plan (ESOP).

While ESOPs remain relatively rare within pediatric therapy, their continued appearance demonstrates that founder succession is not limited to private equity or strategic acquisitions. Since 2017, only a handful of pediatric therapy organizations have completed ESOP transactions, making employee ownership an alternative worth considering for founders whose objectives extend beyond maximizing purchase price alone.

Geography Still Matters

Transaction activity continues to concentrate in markets with attractive demographic and economic characteristics.

States such as Texas, Florida, North Carolina, Virginia, Arizona, California, Colorado, and Illinois continued to appear prominently among acquired providers during the last twelve months ended June 2026. These markets generally benefit from combinations of population growth, expanding pediatric populations, favorable demand trends, opportunities for consolidation, and an established presence of larger pediatric therapy organizations.

Geography alone does not determine acquisition interest, but market characteristics increasingly influence buyer priorities, particularly as investors become more selective in capital deployment.

Quality Has Become More Important Than Growth Alone

Perhaps the most significant takeaway from the current market is not the number of transactions completed, but how buyers are evaluating opportunities.

Several years ago, rapid revenue growth often attracted considerable buyer attention even when operational infrastructure remained underdeveloped. Today’s market is different.

Buyers continue to pursue growth, but they are placing greater emphasis on operational quality. Factors such as clinician retention, utilization, scheduling efficiency, reimbursement mix, compliance infrastructure, financial reporting, and management depth increasingly influence both buyer interest and valuation.

Founders considering a future transaction should recognize that preparation now extends well beyond increasing revenue. Businesses that demonstrate sustainable earnings, scalable operations, and strong organizational infrastructure are generally better positioned to attract multiple buyers and negotiate favorable transaction terms.

Looking Ahead

The first half of 2026 suggests that pediatric therapy remains one of the more active healthcare services sectors for mergers and acquisitions.

Although the extraordinary transaction environment of 2021 is unlikely to return in the near term, current activity demonstrates that buyer interest remains healthy. Existing private equity-backed platforms continue to expand, new financial sponsors are entering the sector, and strategic buyers remain active participants.

The market has become more selective, not less active.

For founders and operators, that distinction is important. Buyers continue to invest in pediatric therapy, but they are increasingly rewarding organizations that combine clinical excellence with operational discipline, financial transparency, and scalable business models.