HOW WE GOT HERE

WASHINGTON, D.C. — The history of autism insurance mandates is substantially the history of one person. Lorri Unumb, a South Carolina attorney whose son was diagnosed with autism in 2002, spent years navigating a system in which ABA therapy — the treatment her son’s doctors recommended — was routinely classified by insurers as educational rather than medical, and therefore excluded from coverage. She became a paid advocate for Autism Speaks, wrote the model legislation that most state mandates are based on, and worked state by state to get it passed. By 2019, when Tennessee issued an insurance department rule that made it the final state to require autism coverage, every state had some form of law on the books.

The achievement was real. Researchers studying claims data in states with and without mandates found that the laws increased both the number of children receiving treatment and the therapy hours for those already accessing care. Access to ABA grew fastest among children from low- and moderate-income families — the population least likely to have been able to afford treatment before mandates. The mandates worked.

They also worked imperfectly, in ways that Unumb — who went on to become CEO of the Council of Autism Service Providers — described as keeping her awake at night. ‘After all of the progress we have made in all 50 states,’ she said after Tennessee’s mandate, ‘still some child will get diagnosed tomorrow and will be unable to afford the treatment recommended by the doctor, notwithstanding being covered by insurance.’ The gap between coverage on paper and coverage in practice has four distinct causes — and understanding them requires understanding four layers of the system: the state mandates themselves, the federal ERISA exemption, the Mental Health Parity Act, and the 2025 regulatory environment.

THE GRADING CRITERIA

The 2025 report card grades each state’s commercial insurance mandate on five factors: whether ABA is a covered benefit, the age limit on coverage, annual dollar caps, whether a medically necessary standard applies, and whether the mandate covers all state-regulated plans. A grade of A indicates no meaningful restrictions — no age cap, no dollar cap, no hour cap, ABA covered as a medically necessary treatment for any insured individual regardless of age. A grade of F indicates either no commercial mandate or coverage so restricted as to be functionally inaccessible for most families.

One important caveat before reading the table: in states where the statutory text includes dollar caps or strict age limits, the federal Mental Health Parity and Addiction Equity Act (MHPAEA) theoretically makes those provisions unenforceable — you cannot apply more restrictive limitations to autism benefits than you apply to comparable medical and surgical benefits. Where parity has functionally voided a restriction, the grade reflects the practical outcome. But in May 2025, the Trump administration paused enforcement of the 2024 MHPAEA final rules, creating genuine uncertainty about which restrictions are actively enforceable and which are not.

![Families in states with the weakest mandates — including Virginia (ages 2–10 only), Maine (under 10), and Florida ($36,000 annual cap) — face coverage that expires long before their child's therapeutic needs do. | Photo courtesy: [attribution]](https://breakingnewsaba.com/wp-content/uploads/2026/03/autism-insurance-article-image-2.jpg)

GAP ONE: THE AGE CUTOFF PROBLEM

The most visible failure mode in the mandate landscape is the age gap. Several states cap coverage at ages far below the point at which many autistic individuals benefit from behavioral support. Maine’s mandate ends at age 10. Rhode Island’s ends at 15. Virginia’s covers ages 2 through 10 — a window so narrow that a child who ages out still has a decade or more of potential developmental benefit ahead of them with no commercial insurance support. South Carolina requires not only that the child be under 16 but that they were diagnosed by age 8 — a combination that makes it the most restrictive mandate in the country by any measure.

The clinical justification offered for early-cutoff mandates is that early intensive intervention produces the greatest developmental gains, and that the economic rationale for coverage diminishes with age. The evidence is more nuanced: the developmental gains from early ABA are real, but the claim that older children and adolescents derive no clinically meaningful benefit is not well-supported in the literature. Many autistic teenagers and adults benefit from ABA in areas — communication augmentation, adaptive behavior, community integration — that aren’t captured in early-intervention outcome studies. The age cutoffs reflect fiscal limits, not clinical ones.

GAP TWO: THE DOLLAR CAP PROBLEM

Florida’s mandate caps ABA coverage at $36,000 per year and $200,000 over a lifetime. Intensive ABA therapy at 25 to 40 hours per week, at rates between $120 and $200 per hour, generates annual costs of $156,000 to $416,000 for a child receiving full recommended dosing. Florida’s annual cap covers between nine weeks and five months of intensive therapy. The dollar caps in Texas, Arizona, Alabama, and South Carolina follow the same pattern: structured to appear meaningful while remaining inadequate for any child with high-intensity clinical needs.

The MHPAEA argument against dollar caps is theoretically sound: if a plan covers a broken leg without an annual benefit cap, it cannot apply a $36,000 annual cap to autism treatment. But enforcing that argument requires a family or provider to file a parity complaint or initiate litigation. Most families do not. Most providers do not have the resources to litigate on behalf of individual patients. The caps persist in statute and in practice for families without the knowledge or means to challenge them.

“Approximately 61 percent of Americans with employer-sponsored health insurance are enrolled in self-funded plans. State autism mandates do not apply to them.”

GAP THREE: THE ERISA LOOPHOLE

The most significant gap — measured by the number of people it affects — is invisible on any state-by-state map. Approximately 61 percent of Americans with employer-sponsored health insurance are covered by self-funded plans, in which the employer assumes direct financial responsibility for claims. The Employee Retirement Income Security Act of 1974 (ERISA) preempts state insurance mandates for self-funded plans. This means that an employee of a company with 500 workers, living in California — which has the strongest commercial autism mandate in the country — may have zero ABA coverage if their employer’s self-funded plan excludes it. The insurance card looks the same. The coverage is not.

Many large employers have voluntarily added ABA coverage to their self-funded plans, particularly after federal MHPAEA requirements made ABA exclusions increasingly difficult to legally defend. As of 2018, Autism Speaks estimated that 45 percent of companies with 500 or more employees covered ABA in their self-funded plans. That figure has grown but has not reached universal coverage. Identifying whether your plan is self-funded requires reading the Summary Plan Description — most families learn about the ERISA exemption only after a claim is denied.

![Families covered by large-employer self-funded health plans may discover they have no ABA coverage only after a claim is denied — regardless of the state mandate in their state of residence. The ERISA exemption is the single largest structural gap in the autism coverage landscape. | Photo courtesy: [attribution]](https://breakingnewsaba.com/wp-content/uploads/2026/03/autism-insurance-article-image-3.jpg)

GAP FOUR: PARITY ENFORCEMENT IN 2025

The 2024 MHPAEA final rules — which would have required plans to provide ‘meaningful benefits’ for mental health conditions including ABA — were partially paused by the Trump administration in May 2025. The pause does not eliminate the core MHPAEA protections enacted in 2008 and 2013. Dollar caps and age limits that are more restrictive than comparable medical benefit limits remain theoretically unenforceable. But the pause signals reduced federal enforcement appetite, and plans that had been preparing to comply with the 2024 standards now face uncertainty about what compliance requires.

State insurance departments retain enforcement authority over state-regulated plans, and states with their own parity laws — California’s is among the strongest — can continue to enforce those protections regardless of the federal pause. Families covered by self-funded ERISA plans have no state regulator to appeal to, and the federal enforcement pause directly reduces the protections available to them.

STATES TO WATCH IN 2026

New York has the strongest mandate in the country but faces the most significant near-term threat to any A-grade state. Assembly Bill A03896 would cap ABA coverage at 680 hours per year — roughly 13 hours per week, below the minimum threshold for most early-intervention cases. Advocates, providers, and families have organized against the bill, which is framed by supporters as expanding access through an alternative therapy model but is widely understood in the provider community as a cost-control mechanism.

Washington state’s HB 2331 is the most provider-protective ABA legislation of the current session anywhere in the country. The bill would require the state Health Care Authority to track ABA wait times, prohibit rate reductions where wait times exceed 30 days, require MCOs to use ABA-trained clinicians to review claims, mandate minimum 90-day reauthorization windows, require prompt payment for clean claims with unit-level denial explanations, and prohibit recoupment demands based on payer system errors.

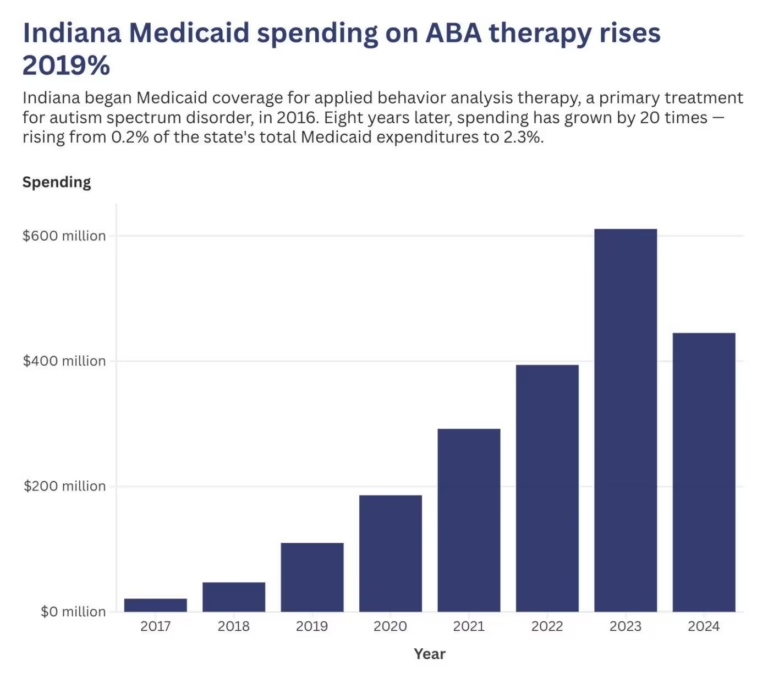

Massachusetts implemented an accreditation mandate in 2025 requiring MassHealth MCOs to contract only with ABA providers holding BHCOE, CASP, or equivalent accreditation — using credentialing as a quality-control mechanism without blunt rate cuts. Indiana’s Medicaid ABA spending crisis creates ongoing regulatory contagion risk: when a state treats ABA as a budget line item rather than a medically necessary benefit, the policy logic tends to migrate from Medicaid toward commercial coverage over time.

![State legislatures across the country are actively moving the mandate landscape — in both directions. Washington's HB 2331 proposes the strongest provider protections in the country, while New York's A03896 would impose a 680-hour annual cap that advocates say would gut coverage for children with the greatest needs. | Photo courtesy: [attribution]](https://breakingnewsaba.com/wp-content/uploads/2026/03/autism-insurance-article-image-4.jpg)

WHAT THE MAP DOESN’T SHOW

The state map is green everywhere. The reality is considerably more varied. A child born today in California, Colorado, Maryland, Kentucky, Oregon, or Washington will grow up with commercial coverage that has no age limit, no dollar cap, and no hour restriction. A child born in Virginia will have commercial coverage only between ages two and ten. A child born in Florida will face a $36,000 annual cap and a $200,000 lifetime cap. A child whose parents work for a large employer with a self-funded ERISA plan — anywhere in the country — will have whatever coverage their employer has chosen to provide.

The mandate campaign succeeded at the policy goal it set: universal coverage on paper. The next campaign — which is already underway in courtrooms, statehouses, and employer benefits offices — is the harder one: ensuring that the paper coverage translates into clinical reality for every family that needs it. That campaign does not have a Lorri Unumb yet. Given what the first campaign accomplished, it needs one.

AT A GLANCE

Coverage Status: All 50 states + DC have enacted autism insurance mandates; applies primarily to fully insured, state-regulated plans

Grade A States (~10): CA, CO, IL (effective), KY, MD, MA, NY, OR, TN, WA — no age cap, no dollar cap, no hour limit

Grade B States (~14): AK, AR, CT, DE, GA, MS, NE, NH, NJ, NM, NC, OH, PA, VT — age limit 18–21, no dollar cap

Grade C States (~17): HI, ID, IN, IA, KS, LA, MI, MN, MO, MT, NV, ND, OK, SD, UT, WV, WI — age under 18 or dollar cap in statute

Grade D States (~8): AL, AZ, FL, ME, RI, SC, TX, VA — severe age restrictions, low dollar caps, or diagnosis-by-age-8 requirements

Grade F States (1): WY — no commercial mandate; Medicaid-only provisions; commercial families unprotected

ERISA Gap: ~61% of employer-sponsored enrollees in self-funded plans are exempt from all state mandates

Most Restrictive: South Carolina — diagnosis by age 8, coverage ends at 16, $50,000/yr cap

Most Protective: California — no age cap, no dollar cap, no hour cap; state parity law reinforces federal protections

Key Threat 2026: NY A03896: 680-hr/yr cap on ABA (pending) — would reduce effective coverage in the strongest-mandate state

Best New Law 2026: WA HB 2331 — wait time tracking, 90-day reauth windows, prompt pay, ABA-trained claim reviewers

Parity Status: 2024 MHPAEA final rules partially paused May 2025; 2008/2013 core protections remain in effect

Federal Pressure: One Big Beautiful Bill Act (2025): $900B+ in Medicaid cuts; compounds state-level access pressure

Coverage Began: 2014 — CMS EPSDT bulletin clarified ABA must be covered under Medicaid; state commercial mandates followed

SOURCES & REFERENCES

1. — Autism Legal Resource Center. State-by-State Autism Healthcare Information. autismlegalresourcecenter.com (accessed March 2026)

2. — Autism Speaks. State Regulated Health Benefit Plans & Self-Funded Health Benefit Plans. autismspeaks.org (accessed March 2026)

3. — Applied Behavior Analysis Education. Autism Insurance Laws by State: ABA Therapy Coverage Guide. appliedbehavioranalysisedu.org (accessed March 2026)

4. — National Conference of State Legislatures (NCSL). Autism and Insurance Coverage State Laws. ncsl.org (accessed March 2026)

5. — U.S. Centers for Medicare & Medicaid Services (CMS). Mental Health Parity and Addiction Equity Act (MHPAEA). cms.gov (accessed March 2026)

6. — Sheppard Mullin Healthcare Law Blog. ‘Enforcement of Mental Health Parity Rules Paused with Further Changes Anticipated.’ May 22, 2025

7. — California Health Benefits Review Program (CHBRP). ‘MHPAEA Explainer.’ October 2025

8. — Autism Policy Blog. ‘ERISA and Autism.’ autismpolicyblog.com (June 2021)

9. — Behavioral Health Business. ‘States Refine ABA Coverage: New Hour Caps, Age Limits, Rate Cuts.’ January 22, 2026

10. — Behavioral Health Business. ‘State Issues to Watch in Autism Therapy: ABA Hour Caps, Rate Cuts.’ March 3, 2025

11. — Disability Scoop. ‘Autism Insurance Coverage Now Required In All 50 States.’ October 1, 2019

12. — Bierman Autism Centers. ‘Insurance Mandates for Autism Spectrum Disorder.’ biermanautism.com (accessed March 2026)

13. — Centria Healthcare. ‘ABA Therapy Insurance Coverage by State.’ centriahealthcare.com (accessed March 2026)

14. — Autism Law Summit. ‘The ABA Authorization and Appeals Playbook.’ 16th Annual Edition, October 2022

15. — Mercer National Survey of Employer-Sponsored Health Plans. ABA coverage in self-funded plans data. 2018. Cited by Autism Speaks

16. — Indiana Capital Chronicle. ‘Governor’s Group Recommends ABA Usage Cap, Rate Changes as Medicaid Costs Rise.’ November 12, 2025

17. — KFF Health News / NPR. ‘It’s the Gold Standard in Autism Care. Why Are States Reining It In?’ December 2025