The Study

Researchers investigated the role of private equity (PE) firms in the rapidly expanding autism services market, specifically focusing on Applied Behavior Analysis (ABA). The study aimed to identify the factors influencing PE acquisition of ABA service delivery sites across the United States, particularly in the context of increasing autism spectrum disorder (ASD) prevalence and robust state and federal insurance mandates for ABA therapy.

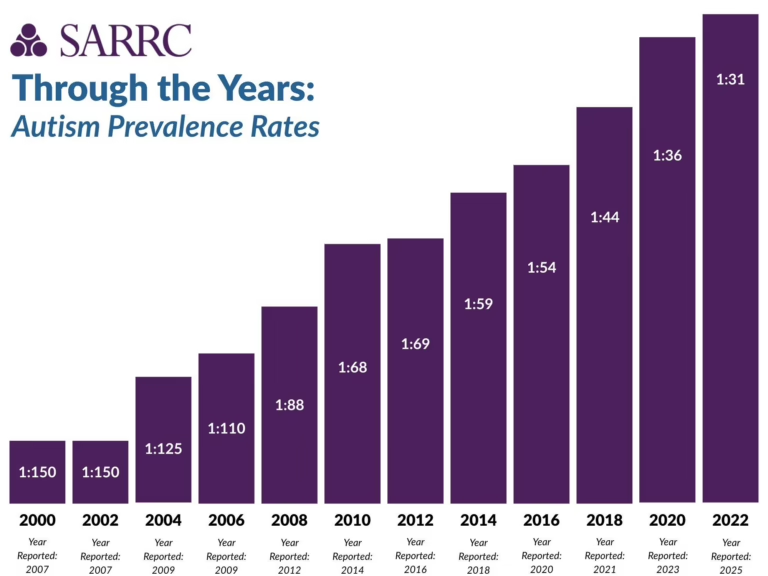

The methodology involved searching PitchBook for PE acquisitions in healthcare containing keywords like “autism” or “ABA therapy services” from January 1, 2015, to December 31, 2024. This initial list was manually verified and expanded using publicly available data. The team then mapped the locations of all PE-owned ASD service delivery sites as of December 31, 2024. These locations were overlaid with state-level autism prevalence data from the Centers for Disease Control and Prevention (CDC) and state autism insurance generosity scores, which ranged from 0 (least generous) to 8 (most generous), based on benefit age limits and spending caps.

To analyze the relationship between these factors and PE entry, a linear probability model was employed using state-year level observations from 2015 to 2022. The dependent variable indicated whether a state experienced PE entry in a given year and subsequent years. Independent variables included an indicator for states in the top tercile of ASD prevalence (14.9 children per 1,000) and an indicator for states with generous autism insurance mandates (score > 4). The model also incorporated state and year fixed effects and controlled for Medicaid expansion status.

Key Findings

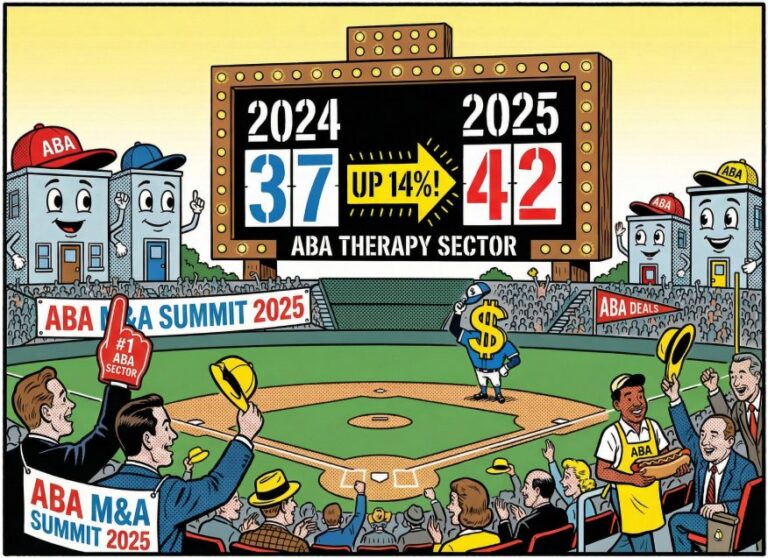

Between 2015 and 2024, the study identified PE-acquired 574 ASD service delivery sites, stemming from 147 distinct acquisitions. The majority of these acquisitions, specifically 79.6% (117 out of 147), occurred rapidly between 2018 and 2022, coinciding with a significant increase in childhood ASD diagnoses. These PE-acquired sites spanned 42 states, indicating a widespread national presence.

The states with the largest number of PE-owned ASD service delivery sites included California (97), Texas (81), Colorado (38), Illinois (36), and Florida (36). Conversely, 16 states had one or no PE-owned sites, suggesting uneven distribution of PE investment across the country.

Regression analysis revealed a statistically significant association between high autism prevalence and PE entry. Being in the top tercile of ASD prevalence was associated with a 24% increase (0.241, 95% CI: 0.078 to 0.405, P<0.01) in the likelihood of PE entry into a state. Visual analysis also suggested that PE firms were more likely to enter states with more generous state autism insurance mandates, although the regression analysis primarily focused on prevalence.

The study acknowledged limitations, including the inability to determine PE’s percentage of the total ASD service delivery sites and the likelihood of undercounting PE acquisitions, a common challenge in tracking private equity activity. Additionally, the precision of coefficient estimates could be affected by limited state-year observations and potential unmeasured confounding variables.

Clinical Implications

The rapid increase in private equity investment in the ABA therapy market, as documented by this study, signals a significant shift in the landscape of autism services. For BCBAs, RBTs, and clinic owners, this trend suggests a growing consolidation within the industry, potentially impacting employment opportunities, compensation structures, and clinical autonomy. The strategic targeting of states with high autism prevalence and generous insurance mandates by PE firms highlights the economic drivers behind these investments, underscoring the importance of understanding payer policies and market dynamics for sustainable practice.

While PE investment can bring capital for expansion and infrastructure, the study explicitly notes that it remains

Source: pmc.ncbi.nlm.nih.gov