Built on Healthcare, Sharpened on Behavioral Health

PITTSBURGH, PENNSYLVANIA – when ABA providers talk about what their company is worth, they are almost always working from a Braff Group number. The firm publishes the most widely referenced quarterly M&A activity reports in the behavioral health space, and its transaction multiples — EBITDA, revenue, and earnings figures compiled from closed deals — have become the de facto benchmark that sellers, buyers, and lenders use when entering negotiations. That market-making function, built over more than two and a half decades, is the foundation of the firm’s standing in the ABA M&A ecosystem.

The Braff Group was founded in 1998 by Dexter Braff, who has served as president since the firm’s inception. The firm focuses exclusively on healthcare services M&A advisory, a narrower mandate than the diversified middle-market banks that compete for the same deal flow. That specialization has proven durable: in a sector where transactions require fluency in Medicaid reimbursement structures, clinical licensing, BACB credentialing considerations, and state-level regulatory environments, generalist banks frequently lack the sector depth that ABA sellers require to command premium valuations.

The firm has completed more than 375 transactions across the healthcare services spectrum, with behavioral health — including ABA, mental health, and substance use disorder — representing a substantial and growing share of its deal pipeline. LSEG, formerly Refinitiv, has repeatedly ranked The Braff Group among the top five healthcare M&A advisory firms nationally by transaction count, a recognition that reflects volume as well as the firm’s sustained activity through market cycles that have included both the early-stage private equity buildout of ABA in the 2015–2019 period and the consolidation wave that followed.

When ABA providers want to know what their company is worth, they are almost always working from a Braff Group number. That market-making function, built over 25 years, is the foundation of the firm’s standing in this sector.

The Bankers: Braff, Weisling, and Garbon

Three names anchor The Braff Group’s ABA and behavioral health practice. Dexter Braff remains the firm’s most public-facing voice on ABA market conditions and valuation. He is regularly quoted in trade media on deal multiples, buyer appetite, and the macro conditions affecting behavioral health M&A, and his commentary functions as something close to a market barometer for PE firms and strategic buyers monitoring the ABA space.

Nancy Weisling serves as a senior behavioral health advisor at The Braff Group and is cited frequently on ABA-specific valuation multiples and market conditions. Her work at the firm sits at the intersection of clinical sector knowledge and transaction advisory, a combination that has become increasingly valuable as buyers conduct more rigorous clinical due diligence before closing ABA deals.

Steve Garbon rounds out the firm’s senior ABA transaction team. Garbon’s deal experience spans the range of ABA company structures — from single-state founder-owned practices to multi-state platforms — and his involvement in transactions signals the kind of deal complexity that requires senior-level advisory attention. Together, the three bring a combination of market visibility, sector relationships, and transaction experience that is difficult for competing firms to replicate in the ABA vertical specifically.

The Data Franchise: Why Braff Numbers Move Markets

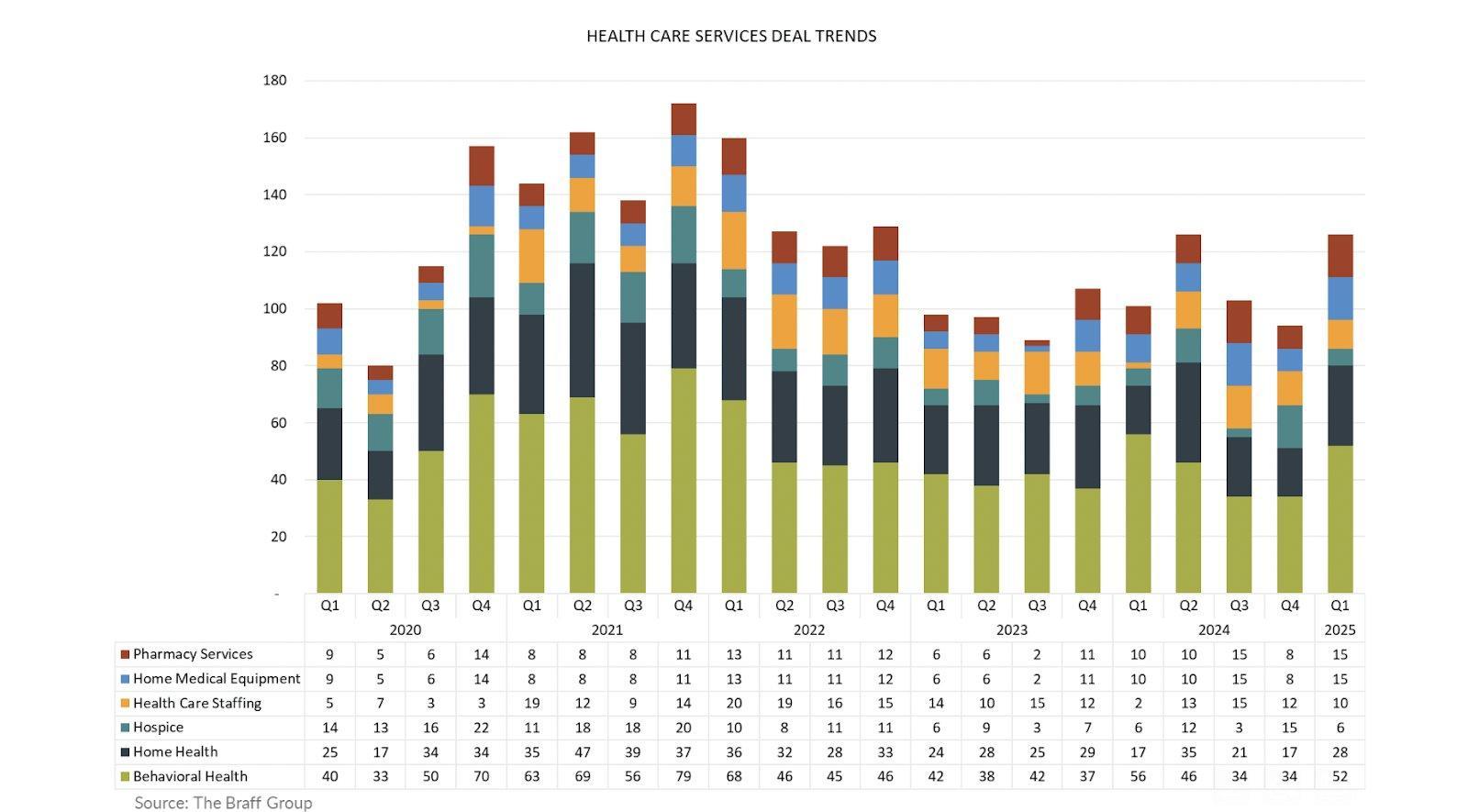

The chart above tells the story in one image. Behavioral health has been the dominant segment in healthcare services M&A for five consecutive years, and The Braff Group’s quarterly tracking of that activity — compiled from closed transactions across ABA, mental health, and substance use disorder — is the primary data series the industry relies on to understand where deal volume is heading.

The Braff Group’s quarterly behavioral health M&A reports are published on a rolling basis and distributed through the firm’s website and industry channels. The reports compile closed transaction counts, valuation multiples, buyer type breakdowns (strategic vs. financial), and deal volume trends across behavioral health subsectors. They do not disclose individual deal terms — most transactions in the ABA space are privately negotiated and not publicly reported — but they aggregate enough transaction data to establish directional pricing benchmarks that both sellers and acquirers treat as credible market signals.

The behavioral health segment peaked at 79 transactions in Q4 2021 — the height of the PE-driven consolidation wave — and contracted sharply through 2022 and 2023 as rising interest rates compressed deal activity across the sector. The Braff Group’s data shows a recovery beginning in Q2 2024 and continuing into Q1 2025, with behavioral health transaction counts returning to the 50–52 range that characterized the pre-peak market of 2020. For ABA providers evaluating exit timing, the trajectory matters: a recovering deal market with active buyer competition is meaningfully different from the contracted environment of 2023.

The practical effect of this data franchise is that The Braff Group enters every engagement with an informational advantage: the firm’s deal flow gives it current, granular pricing intelligence that founder-owned sellers and even sophisticated buyers cannot easily replicate through third-party research. For an ABA provider evaluating exit options, retaining an advisor with access to real transaction data — not published estimates — translates directly into negotiating leverage at the letter-of-intent stage.

The firm’s affiliation with the National Behavioral Health Association of Providers (NBHAP) has further extended its visibility in the ABA market. NBHAP membership and conference presence put Braff advisors in direct contact with the provider organizations, state associations, and advocacy networks that collectively represent a significant share of the acquirable ABA provider base.

Market Positioning: What Braff Does and Doesn’t Do

The Braff Group operates in the lower middle market, a deal size range that maps well to the ABA sector’s ownership structure. Most ABA companies that reach the M&A market are founder-owned, have revenues between $5 million and $50 million, and are being sold for the first time. These are exactly the transactions for which sector-specific advisory creates the most value: the seller lacks M&A experience, the buyer requires confidence in the regulatory and clinical structure of what they’re acquiring, and the pricing outcome depends heavily on how well the advisor can run a competitive process.

The firm does not typically compete for the largest platform transactions — the nine-figure deals involving national ABA operators — where bulge-bracket or large middle-market banks dominate. Its competitive advantage is concentrated in the $10 million to $60 million transaction range, where healthcare-specific expertise and sector relationships matter more than balance sheet or brand recognition. In that range, Braff has no obvious peer in the ABA vertical.

For ABA practice owners considering a sale, The Braff Group’s positioning offers a specific value proposition: a firm that understands ABA-specific EBITDA adjustments, has active relationships with the PE firms and strategic buyers currently acquiring in the sector, and can credibly run a process that generates multiple offers rather than a single-buyer negotiation.

AT A GLANCE

Firm: The Braff Group — Pittsburgh, PA

Founded: 1998

Founder / President: Dexter Braff

Key ABA advisors: Dexter Braff (President); Nancy Weisling (Senior Behavioral Health Advisor); Steve Garbon

Transactions completed: More than 375 healthcare M&A transactions (firm-reported)

Rankings: Repeatedly ranked top 5 healthcare M&A advisory firm nationally by LSEG (formerly Refinitiv)

Sector focus: Healthcare services M&A exclusively; behavioral health (ABA, mental health, SUD) a major vertical

Data product: Quarterly behavioral health M&A activity reports — most widely cited deal data in the ABA sector

Behavioral health deal peak: 79 transactions, Q4 2021 (Braff Group data)

Q1 2025 behavioral health deals: 52 transactions — recovering toward pre-peak 2020 levels (Braff Group data)

Industry affiliation: National Behavioral Health Association of Providers (NBHAP)

Deal size sweet spot: Lower middle market; strongest competitive position in $10M–$60M transaction range

SOURCES & REFERENCES

1. – The Braff Group. Firm overview and transaction history. braffgroup.com (accessed March 2026)

2. – The Braff Group. Health Care Services Deal Trends chart, Q1 2020–Q1 2025. Behavioral health transaction count by quarter. braffgroup.com/mergers-acquisitions-reports

3. – The Braff Group. Behavioral Health M&A Quarterly Reports. braffgroup.com/mergers-acquisitions-reports (recurring publication)

4. – LSEG (formerly Refinitiv). Healthcare M&A advisory rankings. lseg.com (recurring annual rankings; The Braff Group cited in top 5 healthcare M&A advisors by transaction count, multiple years)

5. – National Behavioral Health Association of Providers (NBHAP). Member directory. nbhap.org

6. – Behavioral Health Business. ABA M&A market coverage citing Dexter Braff and Nancy Weisling on ABA valuation multiples and market conditions. bhbusiness.com (multiple articles, 2022–2025)